Module

Category Watch

Leverage always-on intelligence and analytics to proactively identify opportunities and manage risks in your categories.

Category Watch

Persistent global uncertainty is severely straining procurement teams, making it increasingly difficult for category managers to stay informed and make agile decisions.

Beroe’s Category Watch, powered by AI and enhanced by human ingenuity, delivers a comprehensive view of your categories through its four specialized sub-modules: Category Insights, Geopolitical Alerts, Benchmarking, and Alerts & Advisories. Align your category strategies, uncover opportunities on an ongoing basis, and navigate market risks with precision.

Category Insights

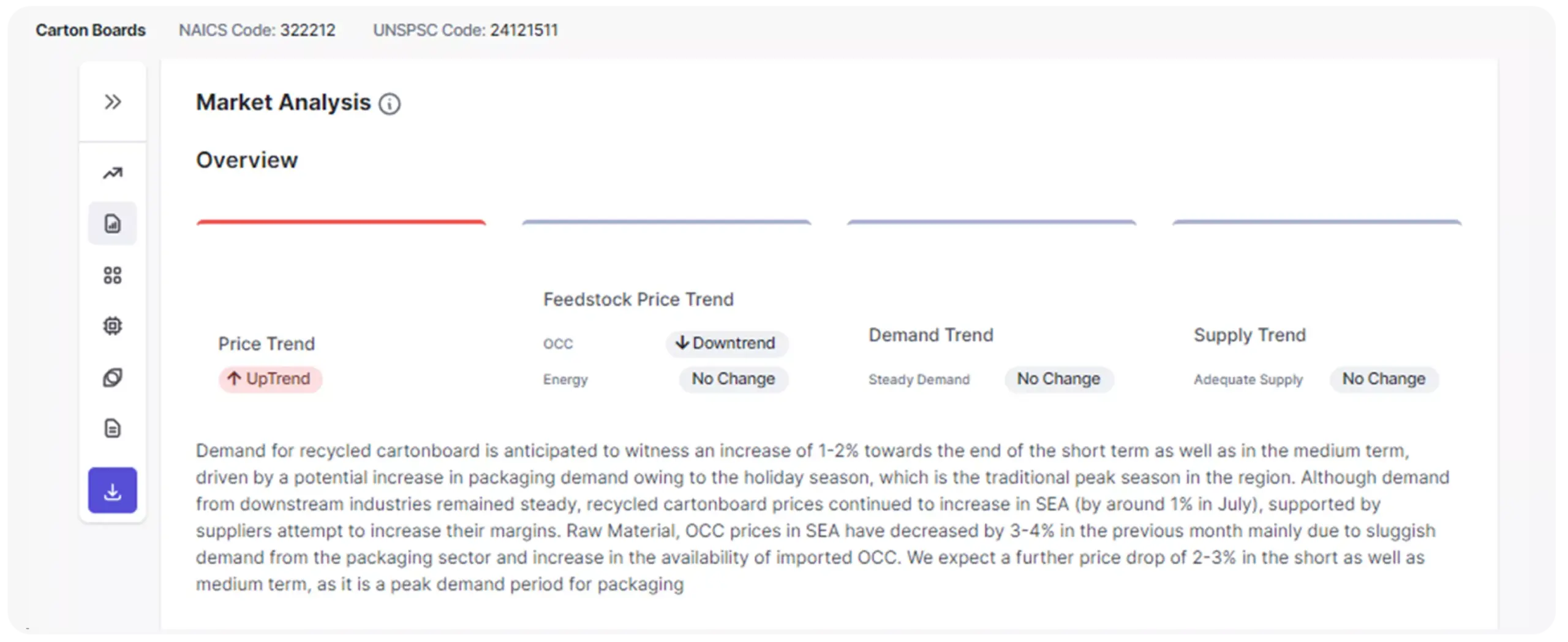

Benefit from in-depth knowledge across more than 3000 categories, gaining a panoramic view of market trends, cost fluctuations, and evolving dynamics to capitalize on cost-saving/avoidance opportunities and minimize risks.

Geopolitical Alerts

Build a robust category strategy by staying ahead of global risks with a 360-degree view of geopolitical and economic factors. Enable procurement teams to identify savings opportunities and avoid material shortages with actionable intelligence that helps smarter category management.

Benchmarking

Evaluate your procurement performance against industry standards with 18 essential questions, uncovering gaps and providing actionable insights to refine your category management practices.

Alerts & Advisories

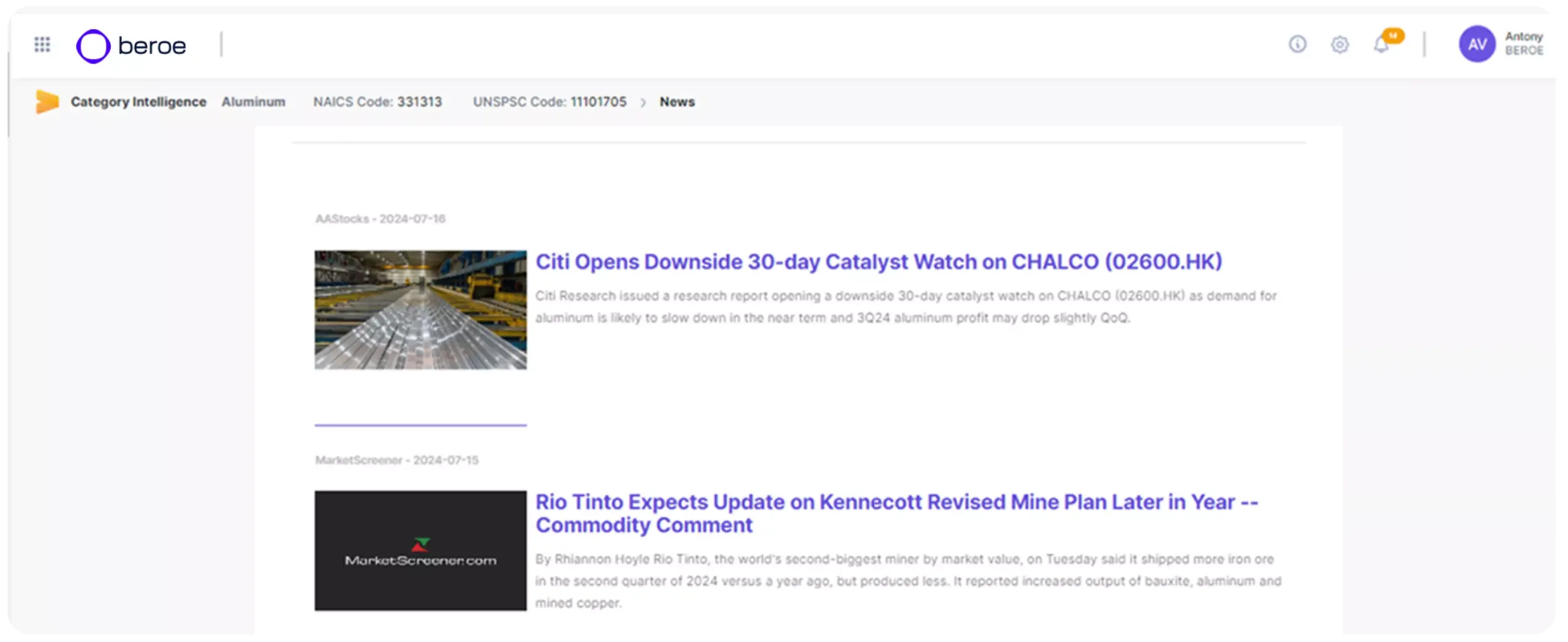

Stay informed with Abi’s timely alerts. Receive daily news, proactive supplier alerts, and strategic insights to adjust sourcing locations, negotiate better contracts, and maintain supply assurance.

3,000

Comprehensive insights into 3,000 direct and indirect categories.

1,000+

Empowering over 1,000 procurement organizations with cutting-edge category intelligence.

40,000+

Engaging with a growing community of more than 40,000 active procurement professionals.

Why Category Watch?

Digital first

Access category updates and insights easily, anytime and anywhere, ensuring you always have the information you need at your fingertips.

Integration of AI and human intelligence

Leverage the perfect combination of AI capabilities and human domain expertise from Beroe providing you with curated insights you can trust.

Actionable insights

Beroe goes beyond data provision. We help you identify market opportunities and risks, empowering category managers to become more resilient and competitive.

Enhanced efficiency

Compare your sourcing practices with those of the Beroe user community across multiple dimensions, such as lead time and cost savings, to identify potential areas of efficiency and better align with business objectives.

Actionable intelligence on more than 3,000 categories

Datasheet

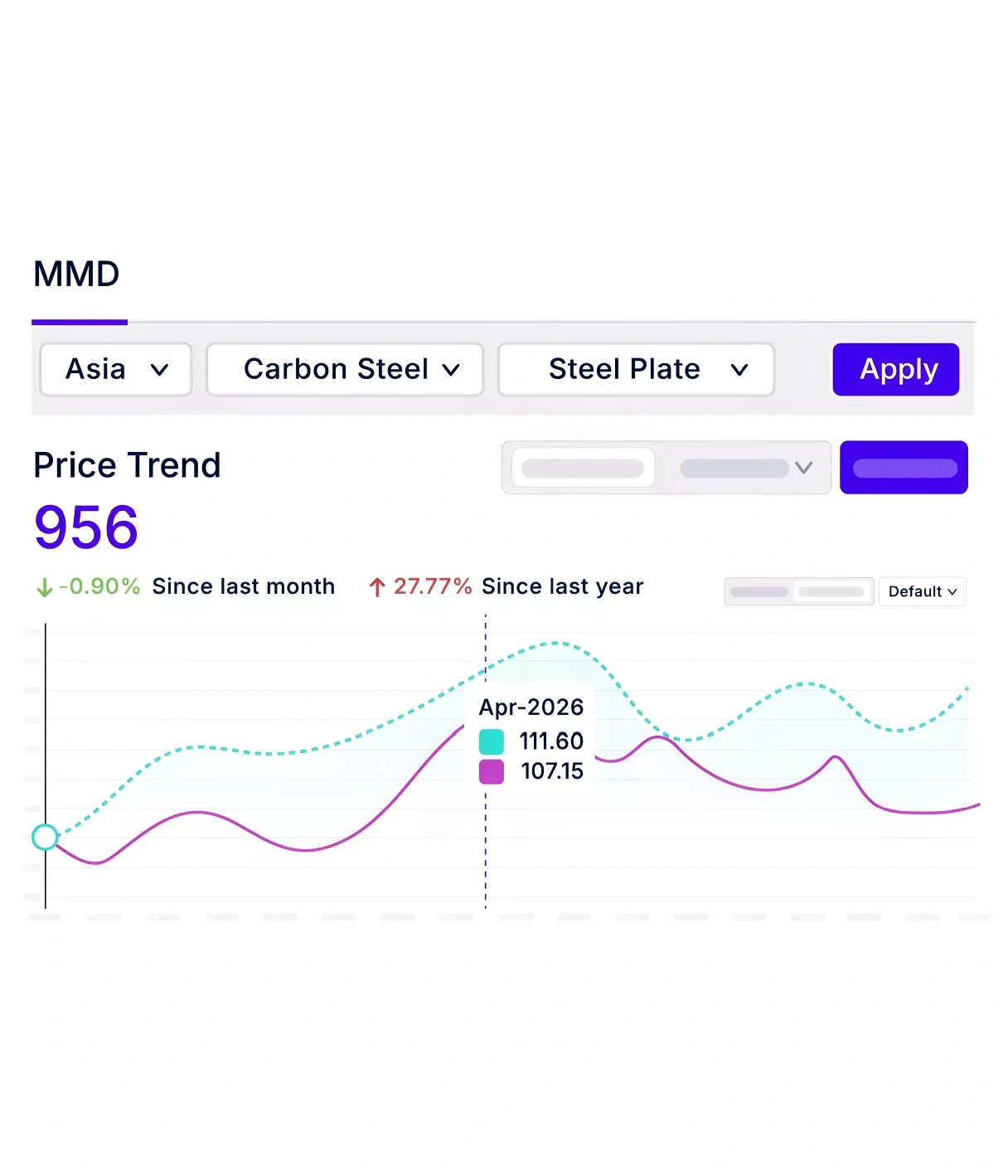

See how the Market Monitoring Dashboard, part of Beroe’s Category Watch module, helps you anticipate price shifts, control costs, and negotiate smarter with data-driven foresight.

Related Resources

Frequently asked question (FAQs)

Category Watch is a procurement intelligence module available on Beroe Live.ai that delivers AI-powered category insights, benchmarking data, geopolitical alerts, and market advisories. With four specialized sub-modules – Category Insights, Geopolitical Alerts, Benchmarking, and Alerts & Advisories – Category Watch empowers you to align strategies, uncover opportunities, and navigate market risks confidently.

It provides detailed cost structures, competitive landscapes, and supply-demand insights to align sourcing strategies with real-time market conditions. Key features include a Category Health Score, which evaluates overall category health across risk, price, availability, and competition parameters.

Category Watch covers 3,000 direct and indirect sourcing categories across global markets.

Yes. It provides benchmarking insights and cost breakdowns to support negotiations and should-cost analysis.

Category Watch provides a 360-degree view of geopolitical and economic factors, helping to identify savings opportunities and avoid material shortages with actionable intelligence. Real-time geopolitical alerts and advisories help procurement teams anticipate supply disruptions.

Get in touch

We’re here to assist you! If you have any questions or need support, don’t hesitate to reach out. Contact us today and we’ll respond promptly to help with your needs.

Request a demo

Discover how our solutions can benefit you. Partner with us to unlock potential and drive success. Let’s work together to achieve outstanding results.