Why Is Affordability Still a Challenge Despite Efficiency Gains?

The global health insurance industry is undergoing a period of rapid transformation. Insurers are investing heavily in AI, automation, and digital platforms to improve operational efficiency, enhance underwriting accuracy, and streamline claims processing. These investments have reduced administrative overhead and improved service delivery across the value chain.

However, these operational gains have not translated into improved affordability for consumers. Healthcare spending continues to rise globally, driven by medical inflation, increased utilization, and rising costs of specialty treatments. Employer-sponsored insurance premiums and out-of-pocket costs continue to outpace wage growth.

This disconnect has shifted the policy conversation. The focus is no longer just on expanding coverage, but on whether insured individuals can actually afford to use their coverage.

This blog analyzes the structural drivers behind the affordability gap, quantifies the disconnect between insurer efficiency and consumer costs, and proposes a practical reform agenda. The scope covers global health insurance markets with a primary focus on U.S. commercial, employer-sponsored, and ACA Marketplace coverage, the segments where the affordability tension is most visible and best-documented.

Why Savings Aren’t Reaching Consumers

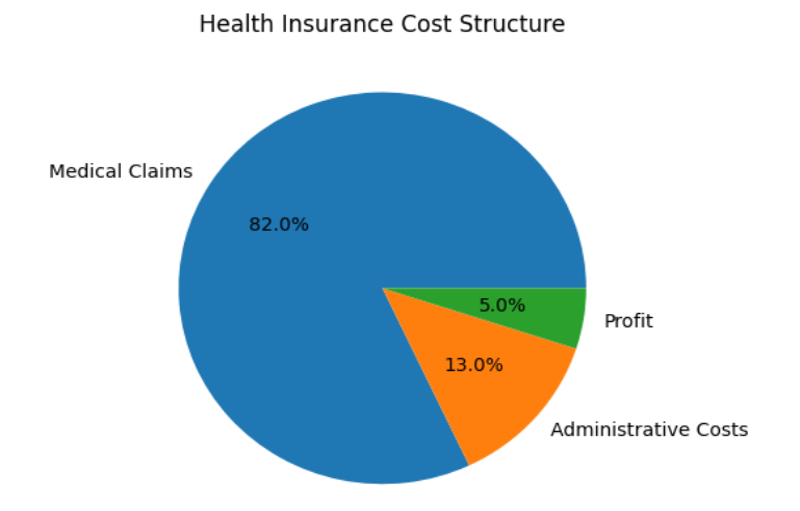

Figure 1:

Source: Umbrex

- Medical Cost Inflation Outpaces Efficiency Gains: Medical costs continue to rise faster than insurers can offset through efficiency improvements. In 2024, U.S. prescription drug spending increased by 7.9% to $467 billion, while hospital spending rose 8.9% to $1.63 trillion [4].

- Efficiency Gains Are Reinvested, Not Passed On: Insurers are reallocating savings from automation into digital transformation programs, compliance and regulatory readiness, customer experience enhancements, and capital reserves, not premium reductions.

- Fragmented AI Deployment: Stuck in “Pilot Purgatory”: Although AI adoption is broad, it is not yet deep. Only a small share of insurers have successfully scaled AI across the enterprise, with most still stuck in pilot phases and fragmented deployments. The result is that the full efficiency potential of AI, compounding savings across underwriting, fraud, claims, and care management simultaneously, remains unrealized for most organizations.

- Provider and Insurer Consolidation: Hospital consolidation is one of the most powerful and underreported drivers of premium growth. When hospitals merge, they gain negotiating leverage over insurers, who then pass higher contracted rates onto employers and individuals through premiums. The FTC has noted that merging hospitals may charge 40-50% more than non-merged competitors [7].

- The Total-Cost Blind Spot-Premiums Are Only Part of the Story: A critical and often overlooked dimension of the affordability problem is that regulatory frameworks and employer benchmarks focus narrowly on premiums, not total consumer cost. A plan can be legally “affordable” under ACA rules while still exposing families to high costs, with average deductibles approaching $1,800-$2,000 for single coverage, excluding additional out-of-pocket spending [9].

- Regulatory Gaps and Administrative Complexity: The ACA’s Medical Loss Ratio (MLR) rule requires insurers to spend at least 80-85% of premium revenue on clinical care and quality improvement activities, limiting the share available for administrative costs and profits [10]. In practice, a peer-reviewed analysis published in the American Economic Journal found that the rule did almost nothing to reduce premiums.

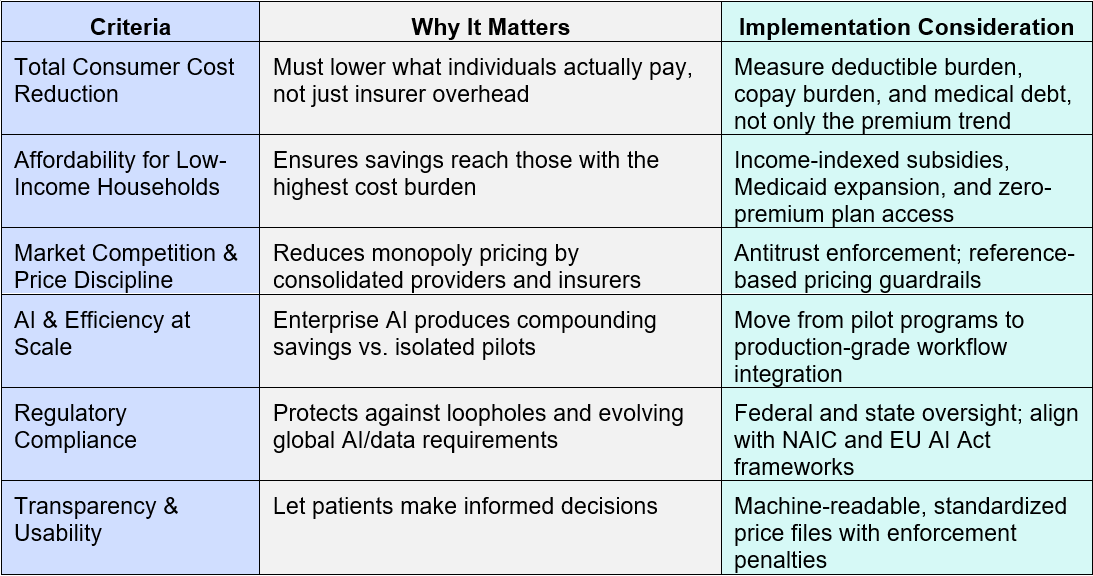

Evaluation Criteria for Solutions

Any credible solution to the affordability paradox must be measured against a clear set of parameters. The most important test is not actuarial: it is whether the solution changes the member’s lived experience. If members still delay care, ration prescriptions, or face surprise bills after implementation, the strategy has failed even if the premium trend improved. The table below captures the full evaluation framework:

Table 1: Key Criteria for Assessing Affordability and Cost-Reduction Strategies

These criteria reflect a core insight from both U.S. and global systems: technical efficiencies alone do not improve affordability unless they reduce what individuals actually pay. For example, Switzerland limits insurer overhead to ~5% of premiums, while Taiwan’s National Health Insurance operates with administrative costs near 1-2%, comparable to traditional Medicare [11] [12]. In contrast, U.S. insurers are permitted to allocate 15-20% of premiums to administrative costs and profit under the ACA (Centers for Medicare & Medicaid Services) [13].

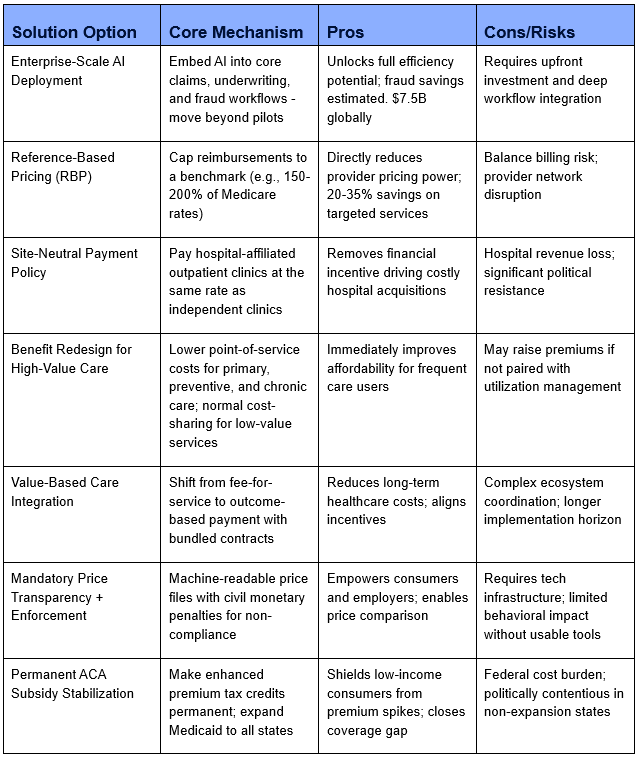

The Shift to “Active Insurance”

No single intervention will unravel decades of structural mispricing and misaligned incentives. The following options are designed as a layered, phased reform stack, not a single silver bullet. The core conceptual shift required is from cost reduction (making the insurer more efficient) to cost translation (ensuring those efficiencies reach policyholders).

Table 2: Evaluation of Health Insurance Affordability Solutions

The Priority Stack: Three Levers That Work Together

In the near term, the most practical path forward comes down to two things that don’t need federal action: scaling AI and rethinking benefit design. Moving AI out of pilots and into core areas like claims and fraud can unlock meaningful, compounding savings, enough to start stabilizing premiums. At the same time, adjusting benefits so that primary care, chronic care, and essential medications cost little to nothing at the point of use, while keeping standard cost-sharing for elective or lower-value services, can make a real difference.

The second layer – price transparency enforcement and reference-based pricing guardrails – is operationally achievable by large employers and self-insured plan sponsors now. Employers who adopt reference-based pricing programs, capping reimbursements at 150-200% of Medicare rates for non-emergency services, have reported average cost reductions of 20-35% on targeted services [14] [15]. The risk of balance billing requires active communication and network management, but newer direct-contract models between employers and regional health systems are addressing this gap.

The third layer – antitrust enforcement, site-neutral payment reform, value-based contracting at scale, and permanent ACA subsidy stabilization – requires regulatory and legislative action but has broad bipartisan support from health economists. Site-neutral payments alone would eliminate the financial incentive driving the most costly form of consolidation: hospital acquisition of independent physician practices.

Recommended Phasing Approach:

The following phased action plan is sequenced by implementation horizon and stakeholder responsibility.

PHASE 1 – Immediate Actions (0-12 Months)

1. Scale AI into Core Operations: Insurers must move beyond pilots and embed AI into production workflows for claims processing, fraud detection, and prior authorization review. Prioritize use cases with the clearest ROI: claims automation and fraud. Establish enterprise-wide ROI tracking so savings are visible and can be formally allocated to pricing decisions, not silently absorbed into margin.

2. Audit Total Member Cost, Not Just Premiums: Employers and plan sponsors should immediately build dashboards measuring deductible burden, copay exposure, medical debt risk, and care deferral alongside premium trend. Without this baseline, affordability claims remain incomplete and reform targets remain invisible.

3. Enforce Price Transparency: CMS should activate full enforcement of the Transparency in Coverage rule, including meaningful civil monetary penalties for non-compliant health systems and insurers. Machine-readable price files must be standardized and made accessible through consumer-facing tools, raw data alone does not change behavior.

4. Bridge the ACA Subsidy Cliff: Congress should pass legislation to extend enhanced ACA premium tax credits beyond their 2025 expiration. Allowing them to lapse is projected to push 4-5 million Americans out of coverage, shifting costs to emergency care and uncompensated pools, raising costs for everyone remaining in the market.

PHASE 2 – Medium-Term Structural Reforms (12-24 Months)

5. Implement a Cost Translation Framework: Insurers and self-insured employers should establish a formal mechanism, a “cost translation policy”, that allocates a defined percentage of documented efficiency savings from AI and automation toward premium stabilization or reduced cost-sharing. This is the missing link between operational efficiency and consumer relief. Target: allocate at least 50% of net operational savings to pricing or benefit improvements in Year 2.

6. Redesign Benefits for High-Value Care: Redesign at least one major plan line so that essential primary care, chronic disease management, and key medications carry near-zero or zero point-of-service cost. Pair with targeted navigation tools embedded in existing member journeys, short, searchable, and mobile-first. The goal: make the lowest-cost clinically appropriate choice the easiest choice for the member.

7. Enact Site-Neutral Payment Policy: Congress should amend Medicare reimbursement rules to pay hospital-affiliated outpatient clinics at the same rate as independent clinics for equivalent services. The Bipartisan Policy Center identifies this as one of the highest-value, lowest-controversy structural reforms available, removing the primary financial incentive driving hospital acquisition of physician practices.

8. Strengthen Antitrust Enforcement for Health Systems: The FTC and DOJ should receive dedicated resources and clearer statutory authority to review and block anti-competitive horizontal and vertical consolidation in health care. Prior-approval requirements for health system mergers above defined market-share thresholds should be codified.

PHASE 3 – Long-Term Market Architecture (24-48 Months)

9. Strengthen Provider Partnerships Through Value-Based Care: Employers and payers should push aggressively toward bundled payments, shared-savings models, and outcome-linked reimbursement so that lower allowed costs generate lower member cost-sharing. A two-year rollout is realistic: Year 1 for data and contract design, Year 2 for pilot and scale. Align provider incentives with utilization efficiency rather than service volume.

10. Redesign the MLR Framework: The ACA’s Medical Loss Ratio (MLR) rule should be reformed to pair percentage requirements with absolute per-member-per-month overhead limits, closing the loophole that allows insurers to inflate the claims base rather than reduce administrative costs. Model this on international examples where overhead caps are paired with defined cost categories and an external audit.

11. Communicate Affordability in Plain Language: Members should see what they are likely to pay for common episodes of care, not only a premium rate and a legal summary. Decision-makers should treat this as a trust project, not merely a pricing compliance exercise. Embed scenario-based cost estimates in open enrollment tools and renewal communications.

12. Expand Medicaid and Close the Coverage Gap: The 10 states that have not adopted Medicaid expansion continue to produce uninsured rates 70% higher than expansion states [21]. Federal incentives or mandates should be pursued to close this gap as a foundational equity and system-efficiency measure.

Insurers, employers, and policymakers need to stop focusing only on internal efficiency metrics and start showing real impact where it matters, what people actually pay. Lower combined ratios don’t mean much if premiums, deductibles, and out-of-pocket costs stay high. Going forward, the real differentiator will be how effectively organizations turn cost savings into visible affordability for members. A good place to start is simple: look at the total cost your members are bearing today, not just premiums. Stay engaged on key policy changes like subsidy extensions and site-neutral payments, because those will directly shape cost structures.

The affordability paradox points to a deeper design issue in today’s health insurance system. Insurers have made real progress on efficiency through digital transformation and AI, those gains are meaningful. But they haven’t translated into what matters most: making healthcare more affordable for people.

Medical inflation, increasing each year, continues to absorb much of these savings. At the same time, AI is often stuck in fragmented pilots, leaving a large share of its potential untapped. Provider consolidation has strengthened pricing power across health systems, limiting how much insurers can push back. Even well-intended regulations like the Medical Loss Ratio haven’t delivered the expected impact. And perhaps most importantly, benefit design has steadily shifted more financial responsibility onto individuals, so much so that even insured consumers, nearly one in four, still struggle to afford care.

Moving forward, insurers, employers, and policymakers must adopt a holistic approach that integrates technology deployment, pricing strategy, benefit redesign, and ecosystem reform. The future of health insurance will not be defined by how much cost is reduced internally, but by how effectively those reductions reach the consumer. Affordability determines whether insurance actually protects people, or merely labels them covered.

References

- Springer Nature, “US healthcare expenditure,” 2025. Available: https://link.springer.com/article/10.1007/s40274-017-3783-4

- KFF, “News Release,” 2025. Available: https://www.kff.org/health-costs/annual-family-premiums-for-employer-coverage-rise-6-in-2025-nearing-27000-with-workers-paying-6850-toward-premiums-out-of-their-paychecks/

- KFF, “Americans’ Challenges with Health Care Cost,” Available: https://www.kff.org/health-costs/americans-challenges-with-health-care-costs/

- KFF, “Hospital Spending Accounted for 40% of the Growth in National Health Spending Between 2022 and 2024”, Available: https://www.kff.org/health-costs/hospital-spending-accounted-for-40-of-the-growth-in-national-health-spending-between-2022-and-2024/

- McKinsey & Company, “Insurance 2030-The impact of AI on the future of insurance”. Available: https://www.mckinsey.com/industries/financial-services/our-insights/insurance-2030-the-impact-of-ai-on-the-future-of-insurance

- AHCJ, “Hospital mergers and health care price increases: A primer for reporters”. Available: https://healthjournalism.org/blog/2024/09/hospital-mergers-and-health-care-price-increases-a-primer-for-reporters/

- AHCJ, “Hospital mergers and health care price increases: A primer for reporters”. Available: https://healthjournalism.org/blog/2024/09/hospital-mergers-and-health-care-price-increases-a-primer-for-reporters/

- IRS, “Publication 974 (2025), Premium Tax Credit (PTC)”. Available: https://www.irs.gov/publications/p974

- KFF, “2024 Employer Health Benefits Survey”. Available: https://www.kff.org/health-costs/2024-employer-health-benefits-survey/

- CMS, “Medical Loss Ratio”. Available: https://www.cms.gov/marketplace/private-health-insurance/medical-loss-ratio

- OECD, “The future of health systems”. Available: https://www.oecd.org/en/topics/policy-issues/the-future-of-health-systems.html

- NLM, “An overview of the healthcare system in Taiwan”. Available: https://pmc.ncbi.nlm.nih.gov/articles/PMC3960712/

- Forbes, “What’s Driving The Cost Of Health Insurance And What To Do About It”. Available: https://www.forbes.com/sites/anthonylosasso/2025/10/28/whats-driving-the-cost-of-health-insurance-and-what-to-do-about-it/

- Rand, “Prices Paid to Hospitals by Private Health Plans”. Available: https://www.rand.org/pubs/research_reports/RRA1144-2-v2.html

- Blue Cross and Blue Shield of Kansas, “The pitfalls of reference-based pricing”. Available: https://www.bcbsks.com/employers/resources/pitfalls-referenced-based-pricing

- KFF, “How Does Cost Affect Access to Health Care”. Available: https://www.kff.org/health-costs/cost-of-insurance-and-its-affect-on-access-to-care-slideshow/

- The Commonwealth Fund, “The State of Health Insurance Coverage in the U.S.” Available: https://www.commonwealthfund.org/publications/surveys/2024/nov/state-health-insurance-coverage-us-2024-biennial-survey

- CEPR, “The High Cost of Living: What Working Families Pay For Health Care”. Available: https://cepr.net/publications/high-cost-of-living-what-working-families-pay-for-health-care/

- Crunchbase, “As Americans Spend More Out Of Pocket On Healthcare, Startups See Opportunity”. Available: https://news.crunchbase.com/health-wellness-biotech/funded-startups-healthcare-out-of-pocket-costs/

- NLM, “US Medical Prices and Health Insurance Premiums, 1999-2024”. Available: https://pmc.ncbi.nlm.nih.gov/articles/PMC12687089/

- KFF, “Key Facts about the Uninsured Population”. Available: https://www.kff.org/uninsured/key-facts-about-the-uninsured-population/?entry=characteristics-of-the-uninsured-population-age

Author

Deepti Sain

Related Reading

22 Jul, 2026

Why AI will make primary research more valuable: A pharma R&D procurement intelligence perspective

20 Jul, 2026

Rebalancing engineering design delivery - onshore vs. offshore strategies in construction procurement