What factors are affecting palm oil procurement in 2026?

Palm oil is a critical input for food manufacturers spanning edible oils, bakery fats, snack foods, and processed foods. Particularly in India, a heavy import dependence (over 60% of edible oil requirements) makes an agile procurement strategy a significant cost and supply risk lever. However, the challenges and opportunities covered here also translate to considerations for palm oil buyers in other global locations.

This blog examines four key dimensions:

- Pricing outlook and scenario-based forecasts under varying Middle East conflict durations

- Supply-demand dynamics influenced by Indonesia’s biodiesel expansion program, biofuel policy shifts, and weather risks

- Trade route assessment and the impact of geopolitical tensions on freight and insurance costs

- Market practices including sourcing strategies, supplier behavior, and negotiation levers relevant to bulk CPG buyers in India

Findings indicate that palm oil prices are driven by elevated crude oil prices, biodiesel-linked demand, and tighter global edible oil inventories. This blog provides actionable procurement recommendations to help food processing companies navigate price volatility, manage supply risk, and optimize sourcing decisions in this environment.

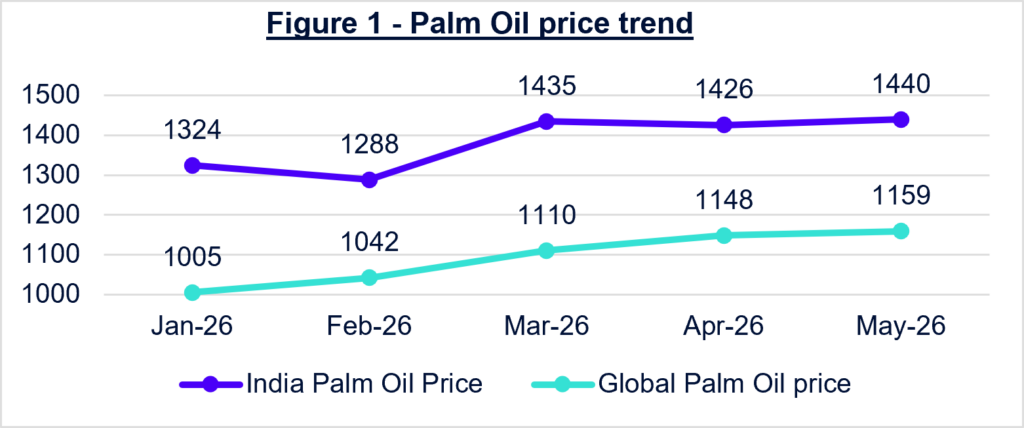

Palm oil price outlook

Global palm oil prices (RBD, FOB Malaysia) recorded a month-on-month increase of 7% in March 2026 and 6% in April, with a year-on-year growth of 15%. [1]

Table 1: Overview of Indian Crude Palm Oil Price Movement 2026 (Scenario Basis)

Source: Oilworld, Solvent Extractors’ Association of India, IMF, Beroe analysis

Indian palm oil prices are expected to stay firm in Q2 and early Q3 2026 at around USD 1,400 to 1,470/MT, supported by elevated crude oil prices. Prices may continue to remain elevated in Q4 if crude oil prices remain elevated. Buyers should secure near-term cover early, phase purchases, and retain flexibility for corrections during seasonal supply recovery. [2] [4] [5]

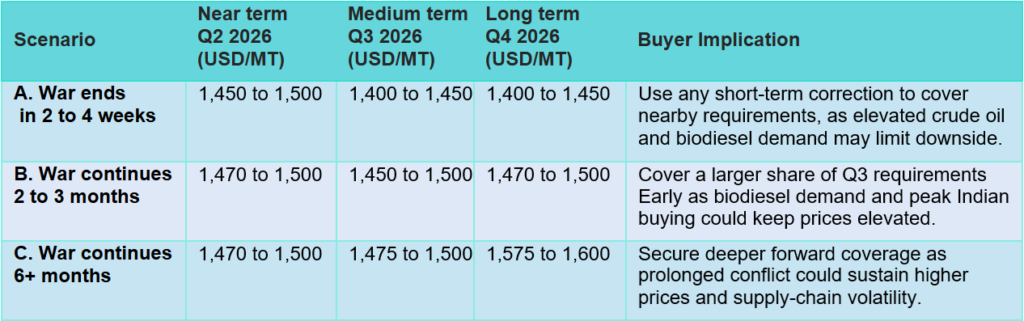

Impact of the Middle East conflict on Indian palm oil

Direct impact on Indian palm oil prices has remained relatively limited compared to global benchmark markets. The major impact has been through higher freight, insurance, and crude oil prices, which supported biodiesel-linked demand and global palm oil prices. Since India imports over 60% of its edible oil requirements, with palm oil forming the largest share, elevated global prices are impacting domestic prices. Prolonged geopolitical tensions could continue supporting prices through higher energy, logistics, and edible oil costs. [4] [5]

Table 2: Scenario-Based Price Outlook

| Scenario | Global Outlook | India Outlook |

|---|---|---|

| A. War ends in 2 to 4 weeks | Prices may see a mild correction, but elevated crude oil prices and biodiesel demand are likely to limit sharp downsides | Prices may remain firm due to import dependence, freight costs, and biodiesel program. |

| B. War continues 2 to 3 months | Higher crude oil prices and biodiesel demand may keep palm oil prices elevated and volatile. | Prices are likely to remain supported due to peak procurement season. |

| C. War continues 6+ months | Sustained energy, freight, and insurance costs may keep palm oil prices structurally elevated. | Prices could strengthen further due to higher landed costs and tighter global edible oil supply. |

Source: Beroe analysis

Indian palm oil supply and demand

Indian palm oil supply-demand is expected to remain broadly balanced, supported by steady imports from Indonesia and Malaysia along with stable domestic consumption growth. However, Indonesia’s biodiesel expansion program, energy inflation, declining palm oil stockpiles in key regions owing to off-season and lower global edible oil inventories are reducing the buffer available to buyers. Key additional risk factors include INR depreciation and USD strength, which increase India’s edible oil import costs, and El Nino-related weather risks that could disrupt palm oil production in Indonesia and Malaysia. [6] [7]

Table 3: Indian Palm Oil Estimates (2025/26, August to July Season)

| Indicator | Value |

|---|---|

| Total Supply | 11.20 MMT |

| Consumption | 9.15 MMT |

| Net Imports | 8.8 MMT |

| eStocks | 2.00 MMT |

Source: USDA PSD Online

Indian palm oil – trade analysis

Indonesia, Malaysia, and Thailand together produce 80% of the palm oil traded in the world, and most of this passes through the Strait of Malacca, the Indian Ocean, the Bay of Bengal, and the Arabian Sea before reaching India. All these pathways have minimal impact from the ongoing war. The major impact is an increase in freight and insurance costs, which have risen by approximately 100% during this period due to geopolitical tensions, elevated crude oil prices, and rerouting risks around the Red Sea region, resulting in higher landed costs for palm oil imports into India. [3]

Table 4: Indian Palm Oil Routes (2025/26, August to July Season)

| Route | Traded Through | Condition | Impact on Indian Palm Oil |

|---|---|---|---|

| Indonesia/Malaysia to India (West) | Strait of Malacca à Indian Ocean à Arabian Sea à Kandla/Mumbai | Open | Low. Major route, uninterrupted. |

| Indonesia/Malaysia to India (East) | Strait of Malacca à Bay of Bengal à Chennai/Kolkata | Open | Low. East coast stable. |

| Thailand to India | Andaman Sea à Bay of Bengal à Kandla/Chennai/Kolkata/Mumbai | Open | Low. Operational with limited disruption. |

| Indonesia/Malaysia to Europe via Red Sea | Strait of Malacca à Indian Ocean à Red Sea to Suez Canal à Europe | Open with restrictions | Low |

| Indonesia/Malaysia to Europe via Cape Route | Strait of Malacca à Indian Ocean à Cape of Good Hope à Atlantic | Open | Low |

| Indonesia/Malaysia to Pakistan | Strait of Malacca à Indian Ocean à Arabian Sea à Karachi/Port Qasim | Open | Low. Pakistan continues steady imports. |

Sources: porteconomicsmanagement, msc, nautilusshipping, thetradevision, marineinsight, asean, tradeatlas,

Palm oil market practices – key value drivers for suppliers

Strategic long-term sourcing partnerships with refiners for supply assurance

Some leading food companies are increasingly strengthening long-term sourcing partnerships with refiners to improve supply assurance, logistics visibility, and procurement resilience amid rising global supply-chain disruptions. Strategic collaboration with suppliers is also helping companies improve inventory planning and shipment monitoring capabilities. [8]

Volume diversification strategy for price risk management

Leading food companies are increasingly adopting diversified sourcing and pricing strategies to manage volatility in global edible oil markets while protecting operational margins. This typically includes a mix of long-term contracts, strategic sourcing, and selective spot market purchases to balance supply security with pricing flexibility. [8]

Buyer negotiation levers and supplier behavior

Buyer Recommendations

- Hold back major coverage in Q2, as off-season supply tightness is pushing prices temporarily higher. Avoid locking in large volumes at current elevated levels. Concentrate buying in Q3 2026, which offers a better entry point as seasonal production recovers and mill utilization peaks at 85 to 90%.

- Maintain a staggered buying strategy and monitor import parity closely to capture favourable buying windows. (Short Term: 1 to 3 months)

- Increase phased forward coverage and diversify sourcing exposure amid tighter supplies. (Mid Term: 3 to 6 months)

Avoid excessive spot dependence and maintain safety inventory due to freight and delivery volatility. (Long Term: 6 to 12 months)

Table 5: Volume Allocation Strategy for Bulk Palm Oil Procurement

| Procurement Practice | Recommended Volume Allocation | Procurement Approach |

|---|---|---|

| Long-term contracts with refiners | 50 to 60% of annual volume | Fixed or formula-linked pricing to ensure stable supply availability and quality consistency and reduce exposure to sharp market volatility. |

| Flexible and strategic sourcing | 25 to 35% of annual volume | Source volumes through flexible procurement and hedging mechanisms to respond to changing market conditions and price movements. |

| Opportunistic spot purchases (Uncommitted Buffer) | 10 to 20% of annual volume | Spot buying during temporary price corrections, inventory liquidation phases, or softer demand periods to optimize procurement costs. |

Source: Beroe analysis

For bulk Refined Palm Oil procurement volumes, a portfolio-based sourcing strategy is generally more effective for balancing supply assurance, procurement flexibility, and price-risk management in volatile edible oil markets.

Supplier diversification and multi-origin strategy

- Over-reliance on a single refiner-importer creates meaningful risk. Any disruption in their vessel scheduling, refinery operations, or credit position directly impacts supply continuity. Buyers should maintain active relationships with at least 2 to 3 refiner-importers across different port catchments such as Kandla, Mundra, and east coast ports to reduce geographic and logistical concentration risk.

Staying ahead of palm oil volatility through smarter procurement

Prices are likely to remain elevated through Q2 and into Q3, with limited downside unless crude oil prices moderate significantly or geopolitical tensions ease. The indirect impact of the Middle East conflict through higher freight, insurance, and energy costs continues to exert upward pressure on landed costs, even as major trade routes remain operationally unaffected. Buyers are advised to adopt a phased, portfolio-based procurement approach. Diversifying across 2 to 3 refiner-importers across multiple port catchments remains essential to mitigate concentration risk. Ultimately, procurement resilience in this market will depend on the ability to balance cost optimization with supply security, anchored by strong refiner relationships, disciplined volume planning, and proactive monitoring of macro and policy signals.

References

[1] “Commodity Markets,” World Bank Group, 2026. [Online]. Available: https://www.worldbank.org/en/research/commodity-markets

[2] “Palm oil prices to remain high as supply may tighten, demand stays robust – analysts,” The Edge Malaysia, 2026. [Online]. Available: https://theedgemalaysia.com/node/803188

[3] “Energy shock and conflict tighten global palm oil supply,” The Edge Malaysia, 2026. [Online]. Available: https://theedgemalaysia.com/node/802170

[4] “Palm Oil Rally Seen Continuing on Biodiesel Demand Boost, Analyst Mistry Says,” Reuters, May 2026. [Online]. Available: https://www.reuters.com/sustainability/climate-energy/palm-oil-rally-seen-continuing-biodiesel-demand-boost-analyst-mistry-says-2026-05-06/

[5] “CPO Prices to Remain above RM4,500 per Tonne on Biodiesel Expansion,” The Star, Apr. 2026. [Online]. Available: https://www.thestar.com.my/business/business-news/2026/04/24/cpo-prices-to-remain-above-rm4500-per-tonne-on-biodiesel-expansion—mpoc

[6] “Malaysia’s March Palm Oil Stocks Hit Seven-Month Low as Exports Surge,” The Star, Apr. 2026. [Online]. Available: https://www.thestar.com.my/business/business-news/2026/04/10/malaysia039s-march-palm-oil-stocks-hit-seven-month-low-as-exports-surge

[7] “Market Report May 2026,” Lipsa, May 2026. [Online]. Available: https://www.lipsa.es/en/market-report-may-2026/

[8] “Inside ITC’s Edible Oil Playbook,” LinkedIn Pulse, 2026. [Online]. Available: https://www.linkedin.com/pulse/inside-itcs-edible-oil-playbook-somnath-chatterjee-procurement-warzf/

Author

Dharshana V

Related Reading

30 Jun, 2026

Direct-to-Consumer Models: Enabling Direct Access to Consumer Healthcare Services

17 Jun, 2026

Navigating 2026: How to Move From Participation to Performance in Corporate Wellness