Secondary aluminum, metal recovered through the recycling of post-industrial and post-consumer scrap, has transitioned from a cost-management instrument to a strategic imperative across the global metals industry. This shift is driven simultaneously by decarbonization mandates, geopolitical fragmentation, and structural cost advantages over primary smelting that now exceed 90% in energy savings per tonne produced. However, the growing reliance on scrap-based feedstock is reshaping global supply chains in ways that introduce new vulnerabilities. Scrap availability is inherently linked to end-of-life material flows and collection infrastructure maturity. At the same time, governments are increasingly treating metal scrap as a strategic resource, implementing export restrictions, tightening contamination standards, and reconsidering trade regimes under carbon border adjustment mechanisms. This emerging scrap nationalism is reshaping global trade flows. [1], [2]

This whitepaper examines the rising significance of secondary aluminum through three interconnected lenses: supply chain structure, protectionist trade dynamics, and industrial implications. It analyses the evolving economics of recycled aluminum, structural constraints on scrap supply, regional trade realignments, and sector-specific impacts. The paper further evaluates how protectionism, decarbonization mandates, and geopolitical realignment may transform secondary aluminum from a sustainability lever into a critical industrial asset.

Introduction: Structural Shift from Primary to Secondary Aluminum

Secondary aluminum offers a structurally lower-energy and lower-carbon alternative to primary smelting. Advances in alloy-level sorting, melt optimization, and circular economy policy frameworks are accelerating adoption across automotive, packaging, and construction sectors. As decarbonization commitments intensify and energy markets remain volatile, competitive advantage in aluminum is gradually shifting away from ore access and electricity pricing toward scrap availability, quality control, and processing sophistication.

The structural shift is driven by three reinforcing dynamics:

- Energy Economics: Electricity price volatility continues to pressure primary smelters, particularly in high-cost regions.

- Carbon Regulation: Recycled aluminum’s significantly lower embedded emissions improve compliance with CBAM and corporate Scope 3 targets.

- Industrial Policy: Governments increasingly support domestic recycling ecosystems to strengthen industrial resilience and reduce import exposure. [3], [4]

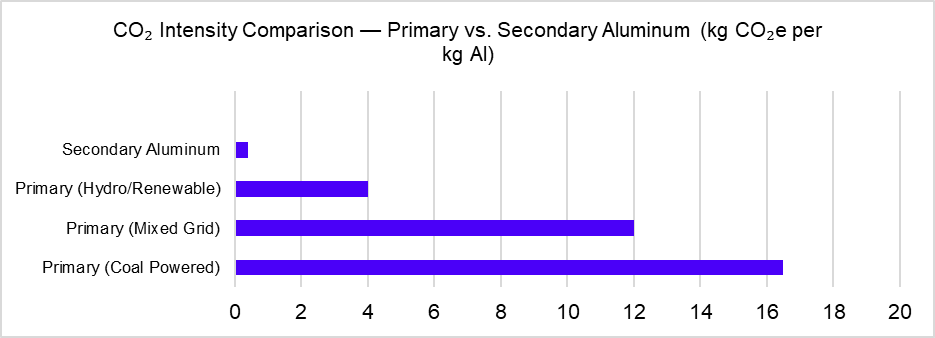

Lifecycle Carbon Economics: Primary vs. Secondary Aluminum

Source: International Aluminium Institute, IEA

- Mandatory carbon disclosure, Scope 3 accountability, and science-based targets have turned aluminum’s carbon intensity from an ESG narrative into a commercial variable.

- The lifecycle emissions of secondary aluminum are typically just 4–5% of coal-based primary production, creating an emissions gap that directly affects procurement strategy. [4], [5]

Mapping the Secondary Aluminum Supply Chain

Global aluminum scrap supply can be segmented into three primary streams, each with distinct quality characteristics, availability profiles, and processing requirements.

| Scrap Category | Global Volume (Mt) (2025) | Share of Total | Avg. Purity Grade |

|---|---|---|---|

| Post-Consumer Scrap | 17.2 | 40-45% | Mixed Alloy |

| Post-Industrial Scrap | 10.4 | 25-30% | High / Known Alloy |

| Old / Obsolete Scrap | 8.1 | 20-25% | Mixed / Variable |

Source: International Aluminium Institute, IEA

- Post-Industrial Scrap: Also referred to as prompt or new scrap, PIS is generated during manufacturing processes, including stamping, extrusion, rolling, casting, and machining.

- Post-Consumer Scrap: Post-consumer scrap arises from products that have reached end-of-life, including used beverage cans (UBCs), automotive components, window frames, appliances, and electronics.

- Obsolete / Long-Life Scrap: Obsolete scrap originates from long-duration applications such as buildings, infrastructure, aircraft, and industrial equipment. [5], [6]

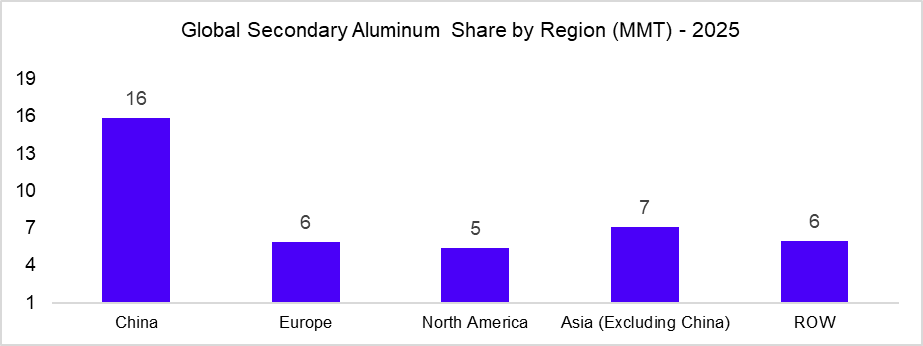

Global Share of Secondary Aluminum

Source: International Aluminium Institute, ALcircle

Secondary (recycled) aluminum accounted for approximately 35% of global aluminum production in 2025, with the remaining 65% coming from primary production. The global aluminum recycling market is expected to expand from about 39.35 million tonnes in 2025 to roughly 41.14 million tonnes in 2026, with continued growth projected through 2030 at an estimated CAGR of around 4.5%. [7], [8], [18]

Protectionism and Trade Policy

Several countries have explored or implemented scrap export restrictions to retain feedstock for domestic recycling industries. If broadly adopted, export controls could fragment global scrap markets, reduce arbitrage efficiency, and widen regional price spreads.

• European Union: Considering measures by 2026 to curb scrap exports and secure recycling feedstock after exports reached ~1.26 Mt in 2024 amid a ~2 Mt domestic scrap shortfall.

• United States: Scrap trade remains open, but pressure is rising to restrict high-grade exports such as used beverage cans due to supply security and China’s recycling expansion.

• India: A scrap-deficit market (~80% import reliance) pursuing lower duties and taxes to expand recycling capacity.

Across jurisdictions, aluminum recycling is becoming central to industrial policy, linking supply security, decarbonization, and circular economy goals. [9], [10], [11]

Technology Frontier Reshaping Secondary Production

- Sensor-Based Sorting: XRF and LIBS systems enable high-precision segregation of mixed scrap, reducing downgrading and unlocking premiums for wrought alloys.

- SmartMelt & Low-Carbon Furnaces: Furnace electrification, melt optimization, and hydrogen-compatible systems aim to reduce direct emissions and improve energy efficiency.

- Closed-Loop Recycling: Automotive and packaging producers increasingly implement take-back systems where post-industrial scrap is remelted and reused in equivalent applications, enhancing traceability and supply stability. [12], [13], [14]

Strategic Recommendations

- Vertical Integration: Large consumers to invest in scrap processing assets or strategic partnerships to secure feedstock.

- Diversified Procurement: Buyers should diversify scrap sources geographically and monitor export policy risks.

- Long-Term Contracts: Multi-year scrap-linked agreements (3–5 years) provide price stability and secure supply.

- Closed-Loop Systems: High-volume OEMs should pursue closed-loop recycling agreements where economically viable.

- Alloy Standardization: Reducing alloy variety improves recyclability, lowers contamination risk, and simplifies carbon documentation for CBAM compliance. [16], [17]

Conclusion

The aluminum industry is entering a phase where the marginal balance of the market is no longer determined by smelter expansion, but by scrap availability. Primary output continues to grow, but under structural constraints, capacity caps in China, energy volatility in Europe, and rising carbon costs in trade-exposed markets. As export controls, CBAM implementation, and industrial sovereignty agendas take hold, global scrap flows are fragmenting, and regional spreads are widening.

In this environment, procurement strategy becomes a source of competitive differentiation. Organizations that proactively secure scrap streams, diversify geographic sourcing, standardize alloy portfolios, and integrate carbon traceability into procurement frameworks will gain an advantage and pricing stability in a tightening environment. In this next phase of the market, scrap is not simply an input to be purchased; it is a strategic sourcing advantage. Those who align procurement strategy with this reality will secure both supply continuity and competitive cost positioning through the next cycle of aluminum growth. [16], [17]

References

[1] “Aluminium,” International Energy Agency (IEA). [Online]. https://www.iea.org/energy-system/industry/aluminium

[2] “EU plans to curb exports of aluminium scrap,” Reuters. [Online]. https://www.reuters.com/business/eu-plans-curb-exports-aluminium-scrap-2025-11-18/

[3] “Aluminium recycling saves 95% of the energy needed for primary aluminium production,” International Aluminium Institute (IAI). [Online]. https://international-aluminium.org/landing/aluminium-recycling-saves-95-of-the-energy-needed-for-primary-aluminium-production/

[4] “EU to keep indirect emissions out of CBAM for metals,” Fastmarkets. [Online]. https://www.fastmarkets.com/insights/eu-to-keep-indirect-emissions-out-of-cbam-for-metals/

[5] “Carbon Footprint of Recycled Aluminium,” International Aluminium Institute (IAI). [Online]. https://international-aluminium.org/wp-content/uploads/2025/10/Carbon-Footprint-of-Recycled-Aluminium-IAI-Document-Final.pdf

[6] “Europe secures 76.3% in aluminium can recycling led by Germany with 99%,” AlCircle. [Online]. https://www.alcircle.com/news/europe-secures-76-3-in-aluminium-can-recycling-led-by-germany-with-99-117361

[7] “China wins the race against the US in aluminium recycling output capacity and expansion,” AlCircle. [Online]. https://www.alcircle.com/news/china-wins-the-race-against-the-us-in-aluminium-recycling-output-capacity-and-expansion-116529

[8] “Recycling body opposes EU scrap aluminium export curbs,” Reuters. [Online]. https://www.reuters.com/sustainability/land-use-biodiversity/recycling-body-opposes-eu-scrap-aluminium-export-curbs-2026-02-02/

[9] “Carbon Border Adjustment Mechanism,” European Commission. [Online]. https://taxation-customs.ec.europa.eu/carbon-border-adjustment-mechanism_en

[10] “Circular Economy Strategy,” European Commission. [Online]. https://environment.ec.europa.eu/strategy/circular-economy_en

[11] “Inflation Reduction Act of 2022,” U.S. Department of Energy. [Online]. https://www.energy.gov/edf/inflation-reduction-act-2022

[12] “Recycling of Aluminium,” AZoM. [Online]. https://www.azom.com/article.aspx?ArticleID=24478

[13] “Advanced multi-sensor sorting for aluminium,” Recycling Magazine. [Online]. https://www.recycling-magazine.com/2026/02/24/advanced-multi-sensor-sorting-for-aluminium/

[14] “Advanced sorting of aluminium alloys thanks to XRF-BS,” Recycling International. [Online]. https://recyclinginternational.com/technology/product-spotlight/advanced-sorting-of-aluminiumalloys-thanks-to-xrf-bs/54858/

[15] “Material Efficiency in Clean Energy Transitions,” International Energy Agency (IEA). [Online]. https://www.iea.org/reports/material-efficiency-in-clean-energy-transitions

[16] “Recycling and sustainability study,” International Journal of Scientific Research and Applications (IJSRA). [Online]. https://journalijsra.com/sites/default/files/fulltext_pdf/IJSRA-2025-3023.pdf

[17] “Recycling,” The Aluminum Association. [Online]. https://www.aluminum.org/Recycling

[18] “Global aluminium scrap tracker 2025: A 41.7Mt backbone under pressure as demand rises 3.87%,” AL Circle, 23 Feb 2026. [Online]. Available: https://www.alcircle.com/news/global-aluminium-scrap-tracker-2025-a-41-7mt-backbone-under-pressure-as-demand-rises-3-87-117391

Author

Sylvia S

Related Reading

23 Mar, 2026

How Geopolitical Shock and Supply Discipline Are Reshaping Petrochemical Procurement in 2026