Tariff escalation, commodity volatility, and lingering semiconductor shortages have collectively pushed the automotive cost base to its steepest climb in a decade. This article quantifies tier-level cost exposure and prescribes a procurement playbook that can claw back 7-9% of a projected +12% cost surge.

Sourcing and supply-chain leaders will find evidence-based levers: multi-sourcing, FTZ duty-deferral, index-linked contracts, and design-to-cost moves that translate macro risk into competitive advantage.

A 12% cost surge – and the bigger risk beneath the surface

A reinstated 25% Section 301 duty on Chinese auto parts now covers $33 billion in annual imports. For a Csegment sedan assembled in the U.S., duty alone inflates costs by +2.3% (Powertrain +1.25%, Electrical & Electronics (E&E) +0.46%, and Body & Structural (B&S) +0.63%). Commodity, freight, and FX add a further +9.7 %, taking the basecase uplift to +12 %.

Original Equipment Manufacturers (OEMs) now contend with a multi-vector squeeze. While the headline effect is a +12% net uplift in finished-vehicle cost for a U.S. assembly plant, the true enterprise risk sits deeper in the supply chain; Tier 2 foundries, stamped-part suppliers, and tier-3 raw-material providers, where visibility is poor and contractual pass-throughs are weak. Failure to quantify and proactively manage these hidden cost drivers threatens margin recovery targets, jeopardizes launch timelines, and undermines ESG-aligned sourcing commitments.

Tariff spiral:

- 25% U.S.– China Section 301 duties on electronics, potential 30 % punitive duty on EV battery packs.

Input-price whiplash:

- Steel +12%, Aluminum +8%, Copper +9%.

Geo-capacity shocks:

- Taiwan earthquake disrupting wafer fabs

- EU quota on press-hardened steel

Pass-through lag:

- Tier-3 raw material hikes surface in OEM purchase-orders with a six-month delay.

ESG overlay:

- EU Carbon Border Adjustment (CBAM) will add $75–90/ton to high-carbon steel from 2026.

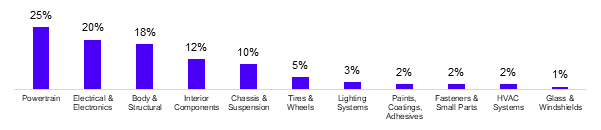

Top spend buckets for automotives

Automotive spend is heavily concentrated across a few critical systems, with powertrain (25%), electrical & electronics (20%), and body & structural (18%) accounting for the majority of total cost. These categories are not only high in value but also deeply exposed to global supply chains, with significant manufacturing footprints in China, India, and Mexico.

Electrical & electronics stands out as the most vulnerable segment due to its reliance on semiconductors, rare-earth materials, and complex sub-assemblies, resulting in very high tariff sensitivity. Meanwhile, powertrain and body systems remain highly exposed to steel and aluminum inputs, amplifying commodity and trade policy risks.

| Tier-1 System | Share | Manufacturing Location | Tier-2 Inputs | Tier-3 Raw Materials | Tariff Impact |

|---|---|---|---|---|---|

| Powertrain | 25% | USA, China, India | Engines, transmissions, turbochargers, exhaust systems | Steel Castings, Aluminum Casting | High |

| Electrical & Electronics | 20% | China, India, Mexico | Sensors, wiring harnesses, ECUs, battery mgmt. systems, infotainment | Electronics, Silicon wafers, copper, rare-earth magnets | Very High |

| Body & Structural | 18% | USA, China | Doors, chassis frames, hoods, roof panels, crash structures | Steel and Aluminum panels, HSS coil, Aluminum billets, epoxy adhesives | High |

| Interior Components | 12% | China, India, Mexico | Seats, carpets, dashboards, instrument panels | Textiles, Plastics, Foam, Leather | Medium |

| Chassis & Suspension | 10% | China, India | Frames, control arms, dampers | Machined steel and aluminum | Medium |

| Tires & Wheels | 05% | China, India, Thailand | Tires, rims, TPMS systems | Rubber, Aluminum Alloys | Medium |

A closer look at price drivers

Powertrain (ICE & Drivetrains)

- 25% duty on Chinese engine castings lifts powertrain bill of materials (BOM) +5 % ⇒ +1.25 ppt COGS.

- Batterycell duty (10 % universal +30% punitive) pushes a 60 kWh pack +7.9% (+$550 / EV).

- NdFeB magnet export curbs would raise emotor cost +12% (+$65 / vehicle).

- FTZ “castinMexico, machineinUS” route defers duty – saving $42/engine for $12 million capex.

Body and Structural (B&S)

- Section 232 steel duty waiver expiry would add +1.6 ppt to Body in white (BIW) cost.

- Midwest aluminum premium at $660/ton lifts extrusions to $71/vehicle (versus $59 in 2022).

- CBAM at €225/ton for highcarbon steel adds $48/vehicle by 2026.

- Five global suppliers control 60% of presshardened steel capacity-concentration risk.

Electrical and Electronics (E&E)

- A 25% duty on Chinese Printed Circuit Board Assembly (PCBAs) raises vehicle COGS by +0.46 ppt.

- Foundry utilization at 87% keeps Application-Specific Integrated Circuits pricing sticky – adds $38/vehicle.

- Scenario: Chinese export curbs would lift EV inverter BOM +6% (+$54).

- Nearshoring engine control unit lines to Mexico defers duty, netting an 18% landedcost cut for $22 million capex.

From tariffs to logistics: Mapping the drivers of automotive cost volatility

| Sl. No | Driver | Mechanism | Recent Trend (2024-Q2) | Relevance to Powertrain, E&E and B&S |

|---|---|---|---|---|

| 1 | Tariffs & Trade Policy | Border duties, local-content mandates | 25% US–China 15% US–EU steel safeguard |

High (imported ECUs, Aluminum stampings) |

| 2 | Commodity Prices | Metals, Resins, Chemicals | HRC +12% y-o-y; Aluminum P1020 +8% |

Critical for B&S steel & Al, Copper traces in PCBs |

| 3 | Semiconductors | Foundry lead times | 22-week average (down from 29) but greater than 2019 | Direct to E&E sub-assemblies |

| 4 | Energy | Grid & gas costs in smelting/foundry | EU power +18% (versus 5-year mean) | Upstream Aluminum & steel production |

| 5 | Freight | Ocean & road logistics | SCFI +9% (post-Red Sea diversions) | Global Tier-2 inflows |

| 6 | Carbon Pricing/CBAM | Import carbon certificates | €90/tCO2e; phased 2026–30 | Direct hit on B&S steel & Aluminum |

| 7 | FX Volatility | Currency swings | CNY +6% versus USD since January 2025 | Tariff savings can be offset by FX losses |

| 8 | Logistics Choke points | Canal & strait disruptions | Panama drought Suez reroutes |

Adds 17–21 days LT, +$140 / FEU |

Impact assessment computation

| Tier-1 System | Spend Share | Import-Content Ratio | Duty Rate | ▲ $/Vehicle | ▲ ppt of COGS |

|---|---|---|---|---|---|

| Powertrain | 25% | 40% (CN) | 25% | +$185 | +1.25 |

| E&E | 20% | 46% (CN) | 25% | +$68 | +0.46 |

| B&S | 18% | 55% (CN/EU) | 15% average | +$101 | +0.63 |

Assumes $30 k vehicle COGS, 1 ppt ≈ $150

Solutions

| Lever | Tactical Action | Target | Benefit | Timeframe |

|---|---|---|---|---|

| Dual / Multi sourcing | Qualify Vietnam & Mexico EMS partners for PCBAs; Add non-Chinese NdFeB magnet supplier | ≤ 50% China spend in E&E by FY-27 | Tariff circumvention, exchange-risk hedge | 6–12 months |

| Nearshoring and FTZ duty drawback | Route Chinese battery cells via U.S. Foreign-Trade-Zone; Export finished packs to Canada | Duty-cash-flow lag < 90 days | 2–3% working-capital relief | 3–6 months |

| Index-linked contracts | Convert fixed BOM pricing to indexed formulas | 90% spend on index clauses | Align cost to market | Immediate |

| Predictive analytics | Map Tier 3 nodes and simulate tariff scenarios | < 72 h alert-to-action cycle | Early warning | Immediate |

Implementation roadmap

- Immediate: Map active Powertrain, E&E and B&S Tier 2 suppliers, overlay tariff codes, build duty-cost dashboard.

- 90-180 days: Execute alternate-source RFQs; negotiate index clauses; pilot multi sourcing program.

- <180 days: Integrate digital twin of supply chain into S&OP; feed scenario outputs into design-to-cost decisions for MY-27.

Conclusion

Tariff-driven cost shocks are no longer episodic; they are a structural feature of the post-2023 trade environment. By quantifying where value is truly created – and where duty, commodity and capacity risks accumulate, OEMs can shift from reactive firefighting to strategic cost-engineering.

Focusing first on Electrical & Electronics and Body & Structural systems captures 38% of vehicle cost and surfaces the bulk of hidden Tier 2/3 exposure. Executing the levers mentioned in this article can recover 7-9% of the 12% tariff hit within 18 months, safeguarding margins and reinforcing supply-chain resilience.

Contact Information

Arun Vijayan

Research Manager

Marquee Team

Author

Arun M Vijayan

Related Reading

02 Apr, 2026

When Power Becomes a Bottleneck: How Energy Constraints Are Reshaping Global Data Center Markets