Something fundamental has shifted in the petrochemical markets heading into 2026. Two forces are now operating simultaneously.

The first is structural: supply discipline, capacity rationalisation across Europe, and escalating trade policy interventions had already begun narrowing cyclical troughs and compressing regional arbitrage opportunities.

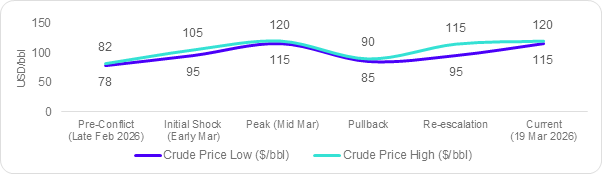

The second is acute. The US-Iran conflict that erupted on 28 February triggered the Strait of Hormuz disruption, supply withdrawal, and abrupt price surges across polypropylene (PP), polyvinyl chloride (PVC), and benzene. What followed was not a single shock and stabilisation. Crude has retraced by a $35/bbl range in under three weeks and sits at $115–120/bbl as of 19 March, with the retaliatory strike on Qatar’s Ras Laffan facilities widening the disruption beyond the Strait itself. [13] [14]

Procurement teams now face both challenges simultaneously, with fewer options than they had at the start of the quarter. Hybrid contracting, multi-origin diversification, feedstock-linked buying triggers, and risk-adjusted cost evaluation are no longer aspirational. They are operational requirements.

Ask most petrochemical procurement teams how they have historically managed this category, and you will hear a version of the same answer: wait for the downcycle, lock in on the trough, and exploit regional price spreads when they open up. The 2024–2026 cycle has been dismantling that logic piece by piece. Supply discipline limited the depth of the correction. European capacity rationalisation reduced supply elasticity. [1] [6] Policy shocks in PVC disrupted trade corridors that buyers had treated as permanent fixtures. [3] [4]

Then, in the final days of February 2026, a geopolitical event compressed years of latent risk into a single week. US and Israeli strikes on Iran, Iranian retaliation, and the effective closure of the Strait of Hormuz produced the supply shock that scenario planners had modelled but many assumed was tail-risk. Prices surged and major producers withdrew March shipment offers entirely. [11] What followed was not stabilisation.

Figure 1 – Crude Oil Price Trajectory (Feb–Mar 2026)

Source: Beroe Analysis

The retaliatory strike on Qatar’s Ras Laffan facilities escalated the crisis beyond initial expectations, removing feedstock and derivative supply that the market had assumed would remain accessible. [13] Gulf storage filled to capacity, forcing output curtailments across the region. [13] [14] The disruption now has no clear resolution timeline. Across all three commodities, prices have continued to climb well beyond the initial shock levels and the scale of the moves is detailed in the sections that follow.

Three Commodities, Three Compounding Crises

The overarching shock is shared, but each commodity carries a distinct risk profile, and the conflict has intensified each in different ways.

Benzene: Arbitrage Closed from Two Directions

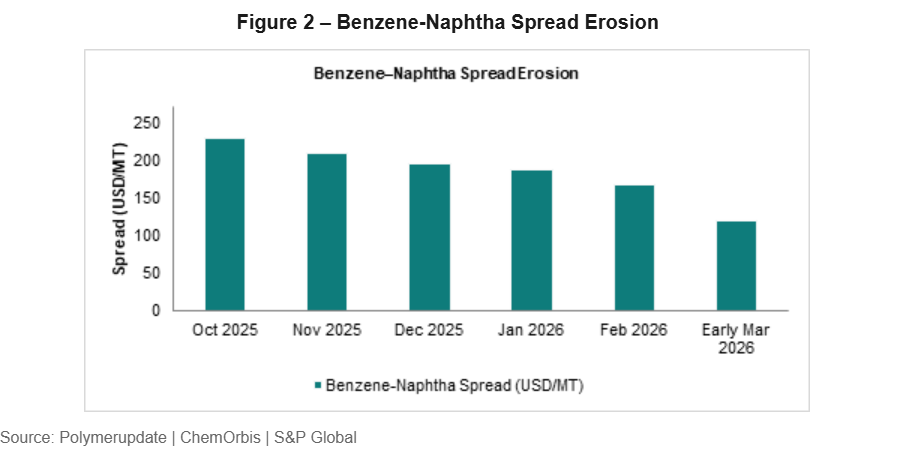

Even before the conflict, benzene’s arbitrage dynamics were deteriorating. The Asia-to-US window had been effectively shut since end-2024 by logistics economics and a 10% US tariff on BTX chemical imports. [2] With the US-Korea benzene premium at $145/MT but tariff plus freight costs consuming that differential entirely, origin switching was already off the table for most Asian sellers. The benzene-naphtha spread averaged $166.81/MT across February before sliding to $118.50/MT in the first days of March. [5]

The conflict restructured the market entirely. Across all three benchmarks, the scale of the move since conflict onset is captured in Table 1a and 1b below. [11] [12] The feedstock chain underpins every regional price move. Naphtha, now up nearly 50% over the past month, [12] has driven a sharp reversal in the benzene-naphtha spread from $118/MT in early March to approximately $290/MT today. This is not margin recovery for downstream buyers. It is cost pass-through from a feedstock chain under simultaneous pressure.

Table 1 a – Benzene Spot Prices

| Product | Unit | Pre-Conflict Baseline | Initial Shock (Early Mar) | Current (18 Mar 2026) |

| Benzene USGC | ($/gal) | 3.04 | 3.04 | 4.09 |

| Benzene Europe | ($/MT) | 885-995 | ~966 | 1,130–1,140 |

| Benzene Asia | ($/MT) | 770-780 | 780 | 1060-1070 |

Source: Polymerupdate | ChemAnalyst | Trading Economics [5] [2] [11] [12]

Table 1 b – Benzene Feedstock Prices (USD/MT)

| Product | Pre-Conflict Baseline | Initial Shock (Early Mar) | Current (18 Mar 2026) |

| Naphtha | ~565 | ~618 | 845 |

| Benzene-Naphtha Spread (Europe) | ~166 | ~118 | ~290 |

Source: Trading Economics | Polymerupdate | ChemAnalyst [12] [11] [5]

In Asia, at least two major Chinese producers cut CDU operation rates by approximately 20 percentage points, with South Korean producers making similar adjustments. [7] Limited spot availability across the region has enabled sellers to raise offer levels consistently. Since the conflict began, Asian benzene prices have risen approximately $300–310/MT in total. [11]

For procurement teams, the arbitrage picture is now doubly closed: structurally by tariff policy, and acutely by conflict-driven freight disruption and feedstock cost escalation. [9] The window that buyers periodically relied upon for origin flexibility does not exist in either direction.

PVC: Supply Withdrawal Deepens Across Multiple Geographies

PVC was already the most policy-exposed commodity heading into 2026. India’s anti-dumping measures against Chinese imports, [3] [4] certification mandate disruptions in Southeast Asia, and structural dependence on Chinese and US export supply had created a fragile trade architecture well before any geopolitical shock.

The initial signal was stark: CFR India PVC jumped $60/MT week-on-week in the first days of March. Chinese sellers, who supplied 39% of GCC s-PVC imports in 2025, rescinded offers, unwilling to risk vessels through the Strait. [10] US sellers (who contributed 41% of GCC imports) withdrew simultaneously, together accounting for 80% of Middle Eastern PVC import supply, both absent at once. [10] [11]

Three weeks on, the market has not corrected. It has extended, as Table 2a shows.

Table 2 a – PVC Spot Prices (USD/MT unless stated)

| Product | Pre-Conflict Baseline | Initial Shock (Early Mar) | Current (18 Mar 2026) |

| PVC Suspension FD NWE (€/MT) | 835–845 | 835–845 | 865–875 |

| PVC Suspension CFR Turkey | 840–880 | 840–880 | 940–980 |

| PVC Suspension CFR Far East Asia | 750–810 | 750–810 | 800–860 |

| PVC Suspension CFR Southeast Asia | 850–900 | 850–900 | 850–1,060 |

| PVC Suspension CFR India | 860–900 | 900–950 | 955–1,100 |

| PVC Suspension CFR GCC | 790–820 | 790–820 | 900–930 |

Source: Polymerupdate, 18 March 2026 (Asia & GCC) | 13 March 2026 (Europe) [11]

The feedstock chain underpins every regional price move. Ethylene, VCM, and EDC have all repriced sharply since the conflict began, as Table 2b details. [11] In Europe, firmer naphtha prices have influenced the April ethylene contract settlement outlook, adding a forward cost pressure layer beyond the immediate spot moves.

Table 2 b – PVC Feedstock Prices (USD/MT unless stated)

| Product | Pre-Conflict Baseline | Initial Shock (Early Mar) | Current (18 Mar 2026) |

| Ethylene FD NWE (€/MT) | 800–810 | 800–810 | 1,055–1,065 |

| Ethylene CFR India | 845–855 | 845–855 | 1,145–1,155 |

| EDC CFR Far East Asia | 240–250 | 240–250 | 295–305 |

| VCM CFR Southeast Asia | 575–585 | 575–585 | 785–795 |

Source: Polymerupdate, 18 March 2026 (Asia) | 13 March 2026 (Europe) [11]

Within this, a structural divergence has formed in the Chinese market. Ethylene-based PVC prices have continued to climb with feedstock costs, while calcium carbide-based PVC prices have softened as buyers remain cautious. This two-tier dynamic limits the degree to which Chinese supply can fill the gap left by Gulf origin withdrawal. [11]

The supply corridor damage extends further. Qatar’s Ras Laffan facilities, struck in the retaliatory escalation, have taken downstream chemical output offline with no clear resumption timeline. [13] Saudi Arabia’s largest PVC unit continues to operate under conflict-premium conditions with export allocations to South Asia suspended. [11]

This is not a temporary pricing disruption. The combination of feedstock cost escalation, corridor disruption, and seller caution across multiple geographies points to a supply architecture that will take time to normalise.

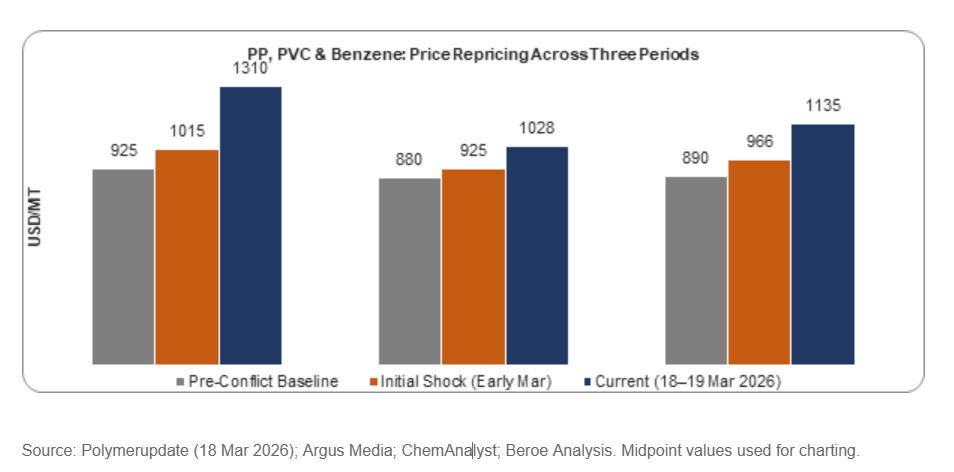

Figure 3 – PP, PVC & Benzene: Pre-Conflict vs. Initial Shock vs. Current (USD/MT)

Polypropylene: Sustained Elevation Across Every Region

PP was in cautious but controlled upward motion heading into March: CFR India raffia at $910–940/MT, propylene FOB Korea at $790–800/MT. [8] [11] One week later, the picture changed completely. PP raffia CFR India jumped $90/MT to $1,000–1,030/MT. [11] Southeast Asian grades surged $70–110/MT depending on specification. [11] Major Middle Eastern and Asian producers withdrew March shipment offers entirely, citing shipping delays and supply-side caution.

Three weeks on, those levels have not held as a ceiling. They have become a floor. Table 3a captures the full regional picture as of 18 March.

Table 3 a – Polypropylene Spot Prices (USD/MT)

| Product | Pre-Conflict Baseline | Initial Shock (Early Mar) | Current (18 Mar 2026) |

| PP Raffia CFR Far East Asia | 1,030–1,060 | 1,030–1,060 | 1,090–1,180 |

| PP Raffia CFR Southeast Asia | 1,020–1,150 | 1,020–1,150 | 1,200–1,330 |

| PP Raffia CFR India | 910–940 | 1,000–1,030 | 1,270–1,350 |

| PP Raffia CFR GCC | 880–960 | 880–960 | 980–1,060 |

Source: Polymerupdate, 18 March 2026 [11]

Table 3b details the propylene moves across key Asian benchmarks. Since the onset of conflict, propylene prices in Asia have risen approximately $305–315/MT [11], the entire cost stack from crude through naphtha, through propylene, through PP has repriced simultaneously and at a speed that quarterly contract structures cannot track.

Table 3 b – Polypropylene Feedstock Prices (USD/MT)

| Product | Pre-Conflict Baseline | Initial Shock (Early Mar) | Current (18 Mar 2026) |

| Propylene CFR China | 915–925 | 915–925 | 1,135–1,145 |

| Propylene FOB Korea | 790–800 | 875–885 | 1,105–1,115 |

| Propylene CFR India | 840–850 | 840–850 | 1,065–1,075 |

Source: Polymerupdate, 18 March 2026 [11]

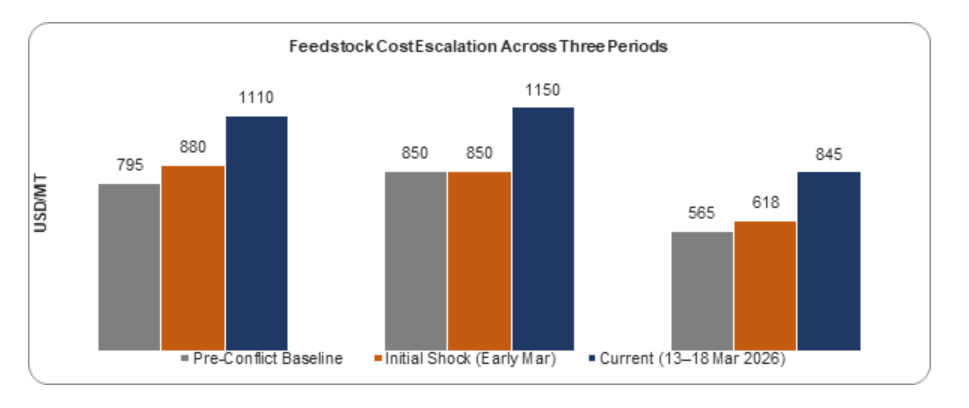

Figure 4 – Feedstock Cost Escalation: Propylene, Ethylene & Naphtha (USD/MT)

Source: Polymerupdate | Trading Economics | Beroe Analysis | Naphtha pre-conflict baseline is estimated [11] [12] [13]

Supply availability remains constrained. Shipping activity through the Strait of Hormuz has slowed significantly, disrupting naphtha and LPG feedstock flows. [13] [14] Several producers have reduced spot and contract allocations, with some informing customers that orders may not be fully fulfilled. The Ras Laffan strike has compounded this, removing Gulf-origin supply that buyers had continued to rely upon even after the initial Hormuz disruption. [13]

Sellers have partially returned to market. Availability is selective, lead times have extended, and the price of accessing supply has risen materially across every origin and grade.

Why Traditional Sourcing Models Are Under Strain

Most petrochemical procurement strategies rest on three assumptions:

- Oversupply eventually produces deep troughs

- Regional spreads widen enough to make geographic switching worthwhile

- Feedstock corrections translate into extended downstream price weakness.

The 2024–2026 cycle has been dismantling all three simultaneously, and the conflict has made each failure immediate rather than gradual.

The first assumption, that oversupply produces troughs, has been undermined by supply discipline that was already compressing corrections before the conflict began. Producer offer withdrawal, not price negotiation, is now the market’s first response to uncertainty. Across PP, PVC, and benzene, the dominant signal over the past three weeks has been the absence of offers, or offers at levels that render quarterly contract benchmarks obsolete.

The second assumption, that regional spreads support origin switching, has broken down across all three commodities. The origins buyers would typically switch to are either unavailable, suspended, or priced at conflict premium. As Figures 1 and 4 show, [13] [12] the entire cost stack from crude through naphtha, propylene, and ethylene has repriced simultaneously, replacing the spread that made switching economically attractive with uniform upward pricing across all available origins.

The third assumption, that feedstock corrections translate into downstream relief, has been inverted. The quarterly contract review cycle, designed for markets where feedstock moves are gradual, now creates a structural lag that exposes buyers to significant unhedged cost risk within a single contract period.

A fourth dynamic has emerged that traditional sourcing models do not account for: the domestic-import price divergence. In India, open market PP and PVC prices have pulled back week-on-week while CFR import costs continue to climb [11],landed cost and domestic market realisations moving in opposite directions, compressing converter margins and creating procurement decisions that cannot be resolved by price alone.

What Procurement Teams Should Do Now

The structural and geopolitical pressures active across benzene, PP, and PVC require action across four dimensions simultaneously. The window for treating these as preparatory measures has closed and each of the four actions below addresses a gap that the current market is actively penalising.

Move to hybrid contracting immediately. Pure spot procurement in PP and PVC is now operating under the worst possible conditions. Offer withdrawal has eliminated the spot discount, and available prices reflect conflict premium, freight escalation, and feedstock cost pass-through simultaneously. Procurement managers should move Q2 volume to hybrid structures: part fixed-price contract, part formula-linked. For benzene, contracts tied to naphtha or crude markers with defined spread floors are preferable to open spot positions given the speed at which the benzene-naphtha spread has moved in both directions over the past three weeks.

Qualify alternative origins before the next disruption. Chinese sellers have partially returned to market but on selective terms. Gulf-origin supply is available in some grades but at conflict premium. Korean, Malaysian, and Taiwanese origins need to be commercially engaged and logistically mapped now. The qualification process takes time that is not available once a disruption begins.

Embed feedstock monitoring into buying triggers. Crude has traced a $35/bbl range in under three weeks. [13] [14] Propylene has moved $305–315/MT since the conflict began. [11] These are intra-period repricing events that require action within days, not weeks. Explicit trigger points such as propylene crossing defined thresholds, benzene-naphtha spreads moving beyond a set range, crude moving beyond a defined weekly band, should automatically initiate a buying or hedging review.

Evaluate cost on a risk-adjusted basis. A lower quoted price from an origin that cannot deliver is not a saving. It is deferred exposure. Risk-adjusted total cost, incorporating origin reliability, freight exposure, war-risk insurance premiums, and corridor risk, must replace simple landed cost comparison as the primary sourcing decision metric. In the current environment, supply certainty carries a premium that belongs in every cost model.

Conclusion

The procurement frameworks discussed in this article (hybrid contracting, origin diversification, feedstock-triggered buying, risk-adjusted cost evaluation) are not forward-looking best practice. The market has provided a live demonstration, at scale and in real time, of what happens when they are not in place.

The conflict has evolved in ways that extend the disruption horizon beyond initial assessments. The retaliatory strike on Qatar’s Ras Laffan facilities has removed supply that was not initially considered at risk. Gulf storage filling to capacity has forced output curtailments across the region. Crude sits at $115–120/bbl as of 19 March with no supply-side resolution in sight. [13] [14]

Buyers that have already moved to hybrid contracting, qualified alternative origins, and embedded feedstock triggers into their buying process are better positioned regardless of how the conflict evolves. Buyers that have not are carrying unhedged exposure in a market where the cost of that exposure is now fully visible in weekly price assessments. If the Strait reopens and the conflict de-escalates, these actions provide resilience at a manageable cost. If disruption extends through Q2 and beyond, which the current trajectory makes increasingly plausible, they may be the difference between protected margins and significant, compounding cost exposure.

References

[1] ChemOrbis, “Europe’s petrochemical industry reshaped by deepening rationalization wave,” ChemOrbis, Sep. 2025. [Online]. Available: https://www.chemorbis.com/en/premium-plastics-news/-Europe-s-petrochemical-industry-reshaped-by-deepening-rationalization-wave-/2025/09/01/944518

[2] S&P Global Commodity Insights, “Benzene and Styrene — Chemical Trends H1 2026,” S&P Global, 2026. [Online]. Available: https://www.spglobal.com/energy/en/news-research/special-reports/chemicals/chemical-trends-h1-2026/trade-flow/benzene-styrene

[3] Polymerupdate, “India imposes anti-dumping duty on PVC Paste resin imports from China and five other nations,” Polymerupdate, 2025. [Online]. Available: https://www.polymerupdate.com/News/Details/1376566

[4] ChemOrbis, “India finally announces ADD on S-PVC imports: What’s in store for subject countries?” ChemOrbis, Nov. 2024. [Online]. Available: https://www.chemorbis.com/en/plastics-news/India-finally-announces-ADD-on-S-PVC-imports-What-s-in-store-for-subject-countries-/2024/11/05/916627

[5] ChemAnalyst, “Benzene Prices, Trends, Chart, Index and News Q4 2025,” ChemAnalyst, 2025. [Online]. Available: https://www.chemanalyst.com/Pricing-data/benzene-25

[6] S&P Global Commodity Insights, “No recovery in sight in 2024 for Europe’s crisis-ridden chemical industry,” S&P Global, Dec. 2023. [Online]. Available: https://www.spglobal.com/commodity-insights/en/news-research/latest-news/chemicals/122923-no-recovery-in-sight-in-2024-for-europes-crisis-ridden-chemical-industry

[7] SunSirs, “Wave of Overseas Ethylene Plant Shutdowns: China’s Ultra-Large Refining and Petrochemical Competitive Edge Reshapes Global Supply Landscape,” SunSirs, 2025. [Online]. Available: https://www.sunsirs.com/commodity-news/petail-28420.html

[8] ChemOrbis, “2025 Polypropylene (PP) Prices, News and Analysis,” ChemOrbis, 2025. [Online]. Available: https://www.chemorbis.com/en/pp/polypropylene-pp-plastics-news-prices-analysis

[9] S. Kalyanasundaram, Beroe Inc., “5 Ways Geopolitical Alerts Help Procurement Teams Navigate the Benzene Market,” Beroe Inc., 2025. [Online]. Available: https://www.beroeinc.com/resource-centre/insights/5-ways-geopolitical-alerts-help-procurement-teams-navigate-benzene-market

[10] ChemDo, “Rumors disturb the bureau, the road ahead of PVC export is bumpy,” ChemDo, 2025. [Online]. Available: https://www.chemdo.com/news/rumors-disturb-the-bureau-the-road-ahead-of-pvc-export-is-bumpy/

[11] Polymerupdate, “Petrochemical Price Reports — Weeks of 27 February, 4 March, 13 March and 18 March 2026,” Polymerupdate, Mar. 2026. [Online]. Available: https://www.polymerupdate.com

[12] Trading Economics, “Naphtha — Price, Forecast & Historical Data,” Trading Economics, Mar. 2026. [Online]. Available: https://tradingeconomics.com/commodity/naphtha

[13] Wood Mackenzie, “The energy crisis is coming to the boil,” The Edge, Wood Mackenzie, Mar. 19, 2026. [Online]. Available: https://www.woodmac.com/blogs/the-edge/the-energy-crisis-is-coming-to-the-boil/

[14] Wall Street Journal, “Oil Futures Rise Amid Widening Middle East Conflict,” WSJ, Mar. 2026. [Online]. Available: https://www.wsj.com/finance/commodities-futures/oil-futures-rise-amid-widening-middle-east-conflict-2af3588d

Author

Swetha Kalyanasundaram

Related Reading

16 Mar, 2026

The New Tariff Reality: How Global Trade Shifts Are Rewriting Electrical Equipment Sourcing