US is currently dependent on imports for several critical links in the battery energy storage supply chain, especially upstream processing and cell manufacturing. Recent regulations could affect supply of critical minerals and battery cells. Industry associations estimate that US domestic suppliers will only be able to meet less than half of the country’s storage demand after the next three years. Procurement teams of companies with energy intensive operations and storage requirements, can take several mitigation measures to ensure supply continuity.

Introduction

China dominates supply of critical minerals and battery cells, which are crucial components of energy storage technology..

US battery manufacturing industry is heavily regulated with multiple frameworks like Resource Conservation and Recovery Act (RCRA), OSHA Standards (Occupational Safety and Health), Extended Producer Responsibility (EPR) Framework, Hazardous Materials Transportation Act (HMTA) and Conflict Minerals Reporting (SEC).

FEOC (foreign entity of concern) poses a new challenge by threatening access to federal incentives and funding, which is critical for economic viability of manufacturers. One Big Beautiful Bill Act preserved full tax credits for the energy storage industry until 2032, but strict FEOC rules deny incentives to projects that are owned or controlled by specific countries. Suppliers can only utilise a certain percentage of minerals or components that are sourced from prohibited entities like China, and the limits tighten progressively after 2029. Domestic battery manufacturers with recent Chinese partnerships might also be affected.

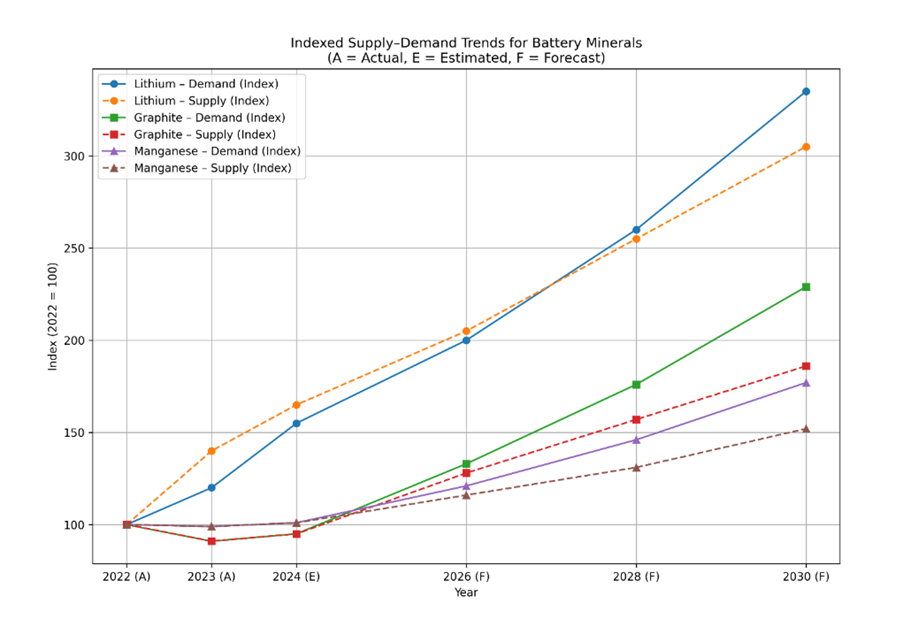

Expected Supply Deficit of Raw Materials

Lithium prices have risen globally on speculations of looming supply shortage by early 2030s. Other raw materials like graphite and manganese are also witnessing a widening supply demand gap, hinting at a potential supply deficit in medium term, depending on demand growth from EV vehicles, grid scale energy storage and consumer electronics. This has already increased forward prices and long-term contract floors. Export controls, processing concentration and qualification for IRA / FEOC-compliance is adding to the effect.

Chart 1: Widening supply Demand gap – Battery production raw materials

Source: US Geological Survey, Raw Materials Information System (RIMS), Energy Metal News

Expected Impact on battery developers

Developers were under pressure to get construction online quickly to avail tax credits before the FEOC implementation in 2026. Going forward limited supply against steady demand growth will raise prices. Some developers will still rely on Chinese batteries raising the overall cost of storage projects.

Several companies have already cancelled or delayed clean energy projects. E.g. Freyr Battery cancelled Giga America Battery Plant (Georgia, 2025), Kore Power cancelled Cell factory plan (Arizona 2025), and Ford (EV manufacturer) suspended battery projects.

Demand for energy storage projects, which are often co-located with renewable technologies is expected to drop by around 10-20 percent by 2030, due to increased complexity in achieving key tax credit subsidising battery production, and earlier phaseout of solar and wind tax credits.

Mitigation Measures

Overall supply may be stabilised by early 2030s driven by early deployments of advanced light-water SMRs (Small Modular Reactors) and inflow of crude based energy from new sources. However, near- to medium-term impact is likely to be higher costs, tighter supply, delayed projects, and more complex procurement strategies. Developers and manufacturers that proactively diversify supply chains, secure long-term contracts, and manage FEOC exposure deep into Tier-2 and Tier-3 suppliers will be better positioned to navigate the transition.

Contracting & Commercial Strategy

Suppliers allocate scarce capacity to committed buyers first. Locking in volumes with 3–7-year contracts is therefore the most effective strategy. This can be supplemented with volume floors and price ceilings, with prices linked to index or the use of price bands rather than fixed prices.

Supplier Diversification

Dynamic geopolitical environment necessitates avoiding concentration of suppliers in any particular geography ( >40-50%). Buyers need to move away from single countries and processing hubs to alternative sourcing locations in US/Canada, Australia, Korea/Japan and select LATAM & Africa (non-FEOC).

Supplier & Supply-Chain Risk Management

Qualifying multiple chemistries such as LFP + NMC, sodium-ion pilots for stationary storage and high-manganese options where feasible, instead of locking into single battery chemistry can reduce exposure to single-mineral bottlenecks (e.g., lithium or graphite).

Exposure Assessment and Monitoring at Tier-2 / Tier-3 level

A Bill of Materials (BOM) risk map visually plotting the security, licensing, and supply chain risks of components is ideal for procurement to assess ownership and exposure at all levels including cell supplier, cathode/anode, and mineral processors, to identify potential refining choke points.

Buyers can include specific contract clauses explicitly enlisting representations & warranties that supplier is not a FEOC, ongoing disclosure obligations if ownership/control changes, audit rights tied to FEOC compliance and termination or remediation clauses if exposure arises due to M&A activities, equity raises or government policy changes.

Inventory Buffer Strategy

Strategic stockpiling of rolling buffers for critical components like cells, anodes, and cathodes, ensuring inventory of 2–4 months for critical SKUs during tight markets, and implementing vendor managed inventories.

Financial Hedging Tools

Prices can be linked to transparent indices, alongside upside caps with collars to manage index exposure. Procurement teams can offer prepayment in exchange for priority allocation, price discounts and expansion capacity rights.

Demand Stabilisation

Demand stabilising methods like demand smoothing and input standardization can be highly effective. Companies can align delivery schedules with supply ramps and avoid sharp volume spikes. Engineering departments can also standardize cell formats and reduce customisation.

Reducing Dependency on Power Storage

Factoring in power supply in major demand centers can reduce dependency on power storage itself. E.g. Power Points US private capital groups KKR and Energy Capital Partners struck a multibillion-dollar partnership to build a data centre with power supplied from Calpine.

Monitoring for early warning signs of shortage

Continuous tracking of lead times, spot vs contract price spreads, policy changes and supplier capex delays can help buyers identify early warning signs of shortage.

Conclusion

FEOC restrictions are set to be a structural inflection point for the US energy storage industry rather than a short-term compliance hurdle. Procurement teams can mitigate potential shortage by locking volume early, diversifying chemistry and geography, and treating supply risk as a financial exposure.

References

[1] [Online]. Available: https://www.eia.gov/todayinenergy/detail.php?id=65305.

[2] [Online]. Available: https://www.iea.org/commentaries/with-new-export-controls-on-critical-minerals-supply-concentration-risks-become-reality.

[3] [Online]. Available: https://www.epa.gov/electronics-batteries-management/extended-battery-producer-responsibility-epr-framework.

[4] [Online]. Available: https://americanli-ion.com/news/us-battery-manufacturing-trends-and-challenges.

[5] [Online]. Available: https://worldreporter.com/battery-supply-glut-looms-as-global-ev-industry-faces-new-pressures/.

[6] [Online]. Available: https://www.congress.gov/crs_external_products/R/PDF/R48538/R48538.7.pdf.

[7] [Online]. Available: https://rmis.jrc.ec.europa.eu/analysis-of-supply-chain-challenges-49b749.

[8] [Online]. Available: https://www.csis.org/analysis/friendshoring-lithium-ion-battery-supply-chain-battery-cell-manufacturing.

Author

Nandhini Dhabathy S

Related Reading

09 Feb, 2026

How Digital Procurement Platforms Are Revolutionizing The Way We Find Suppliers

02 Feb, 2026

Managing volatility: Predictive Commodity Risk Management for Diesel and Gasoline