Managing Tail Spend in Legal Services | Beroeinc

Abstract

Introduction

Managing tail-end spend has become one of the burning issues in recent times for organizations. While the focus is on achieving better efficiency and effectiveness from the “final 20 percent” of spend, determining tail-end spend is more important. The classic approach involves conducting spend analysis and then ranking suppliers based on annual spend. If the total business from smaller suppliers adds upto 20 percent of the total spend, it is defined as the tail. Organizations have often dismissed this part of the spend as insignificant on grounds that accrued cost-savings are negligible. As a result, this spend has been poorly managed. However, in recent times, organizations are considering tail-end spend as a significant source of savings.

The aforementioned problem has plagued the legal industry as well. Tail-end spend has remained as a “blind-spot” as corporate legal departments are always focused on gaining significant cost-savings. Corporate legal departments dedicate a significant amount of their outside counsel spend (80 percent) to core law firms (primary and secondary law firms), which are about 9-11 in number for Fortune 500 companies. The other 20 percent of the spend is concentrated on the other secondary law firms (about 25-30). While the visibility into this spend is little, it is an opportunity which can be explored to achieve significant cost-savings.

This whitepaper will provide insights on how significant the need is in an organization to manage low value spend, challenges faced in arriving at tail end spend, benefits of tail-end spend management and how tail-end spend can be managed effectively in the legal purview.

Problem statement

Tail-end spend contains a small part of the spend (10-20 percent under each spend category). However, a large number of suppliers fall under this bracket and it is comprised of low value purchases. It can have a substantial impact on the financial performance of a firm by enhancing the bottom-line through improved spend under management (30-70 percent), reduced discretionary spend (15-20 percent), transaction count (45-55 percent), reduction in vendor count (20-30 percent), etc. This spend is often poorly managed by firms on the assumption that returns are negligible compared to the vast amount of resources to be used. Consequently, they fail to explore substantial cost-savings within it.

This whitepaper will propose a solution for the following questions :-

- Why is tail-end spend management required?

- What are the challenges faced by organizations to arrive at tail-end spend management?

- Which are the processes that can be adopted to effectively manage tail-end spend?

- What are the benefits of tail-end spend management?

- Which is the category for tail-end spend management within legal services?

Requirement for tail-end spend management

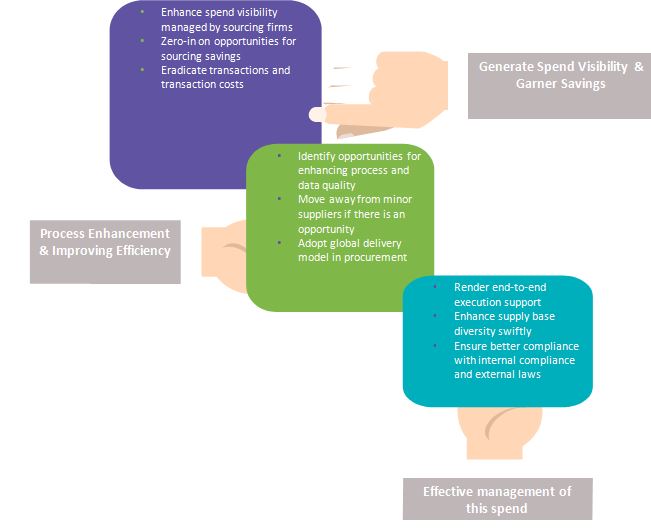

There is increased pressure on organizations to manage escalating costs more effectively and ensure that there are sustained savings which can be achieved. Consequently, more and more organizations are taking closer look on managing their tail-end spend more effectively. The rationale behind organizations resorting to this step as an effective way to reduce costs can be narrowed down to the following:

Challenges faced by organizations to arrive at tail-end spend

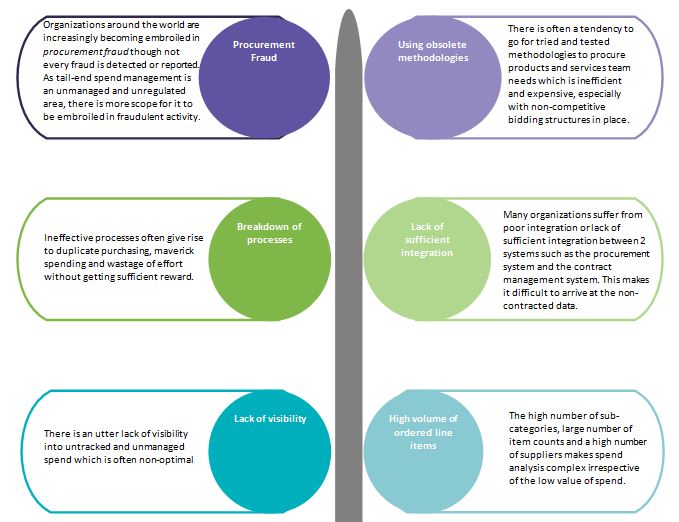

Tail-end spend is often unmanaged and unregulated and there are sufficient cost-savings opportunities hidden in it which can drive an organisation’s efforts to increase spend visibility and cut down on expenses. Organizations often face problems related to “poor data quality” while trying to segragate tail-end spend. This includes incorrect supplier and material names, absence of data linkages, and duplication of data. There are other significant challenges which organizations face with regard to arriving at or managing this tail-end spend:

Procurement Fraud - As an organization grows, its sourcing and purchasing operations grows hand-in-hand providing hard to resist opportunities for employees and suppliers to gain financially through fraudulent malpractices. Procurement fraud is one of the ways in which in-house procurement professionals or corrupt suppliers can achieve financial gains by adopting common fraudulent malpractices such as false invoicing, bid rigging and conflict of interest.

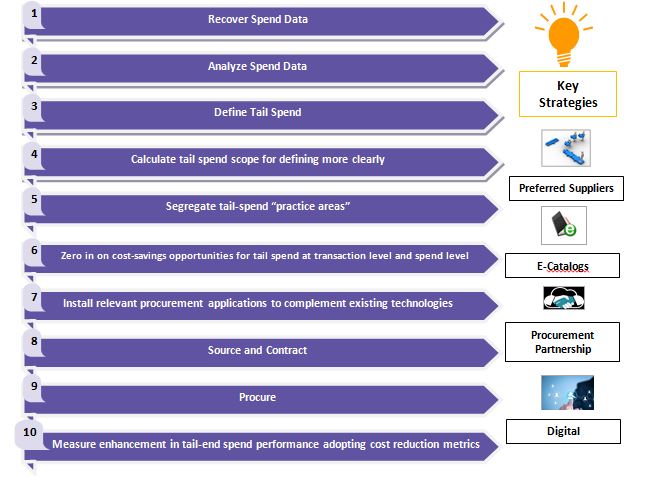

Process to effectively manage tail-end spend

A proper mechanism should be there in place to manage tail-end spend more effectively. The aforementioned steps, if carried out will ensure that the diverse tail-spend categories and sub-categories can be managed more effectively. Companies should also look at adopting strategies to maximise savings hand-in-hand with managing tail-end spend. They can look at diverse strategies such as having preferred suppliers for a mutually beneficial relationship or adopting e-catalogs for enhanced purchasing standards or coming up with a data trail for spend activity.

Insight for Category Manager

Apart from the aforementioned steps which can be adopted to manage tail-end spend effectively, category managers can also look at quality management techniques such as RCA (Root Cause Analysis), PFMEA (Process Failure Modes and Effects Analysis) and value stream mapping combined with procure-to-pay tools (such as Ariba Buyer).

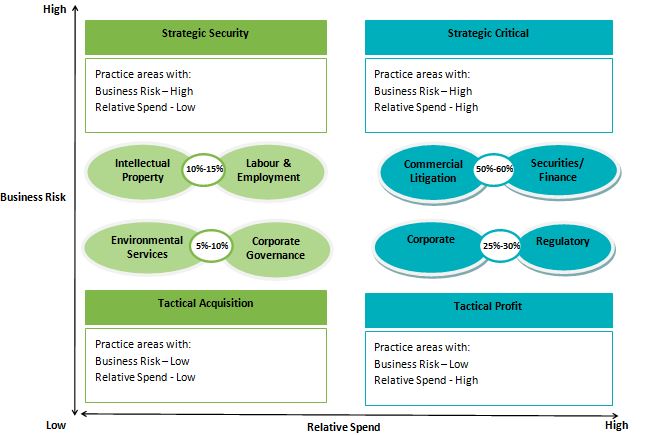

Sourcing strategy framework for tail-end spend management – legal services context – (pharmaceutical industry)

Source: Beroe Analysis

A sourcing strategy framework can be drawn up like the one above, wherein for each practice area the business risk score and spend is listed. A 2x2 matrix is drawn up where spend is kept on the X-axis and business risk on the Y-axis. Procurement goals are zeroed-in on for each quadrant and plans are executed to meet the goals. Using the above quadrant, a decision can be arrived at with regard to practice areas that need immediate attention followed by others.

The percentages indicate the approximate spend (budget) allocated for each practice area falling under different quadrants. For e.g.: the strategic critical quadrant comprising of the IP and employment labour practice areas comprise the highest spend for a typical pharmaceutical company as a lot of patent filing and prosecution matters take place.

Sourcing strategy framework for tail-end spend management – legal services context – (financial services industry)

Source: Beroe Analysis

For the financial services industry, the strategic critical quadrant consists of commercial litigation and securities/finance practice areas. These constitute the highest spend for a typical company based in the financial services industry as a lot of litigation activity takes place arising out of commercial disputes in the financial sphere.

The sourcing strategy framework varies by industry as has been elucidated in the above 2 examples. In case of the manufacturing industry, we would have Litigation and Intellectual Property practice areas in the Strategic Critical quadrant (50-60 percent), Corporate and Securities/Finance in the Strategic Security quadrant (10 -15 percent), M&A and Regulatory in the Tactical Profit quadrant (25 -30 percent) with the Environmental Services and Corporate Governance practice areas rounding off the Tactical Acquisition quadrant (5-10 percent).

Effective ways of managing tail-end outside counsel spend

Corporate legal departments face many challenges with regard to effectively managing tail-end outside counsel spend. These law firms, which fall in the “other”law firm segment after the core law firms (primary and secondary law firms) contribute about 20 percent of the outside counsel spend and warrant different ways to effectively manage them. Some of the methods of achieving this purpose have been highlighted below:

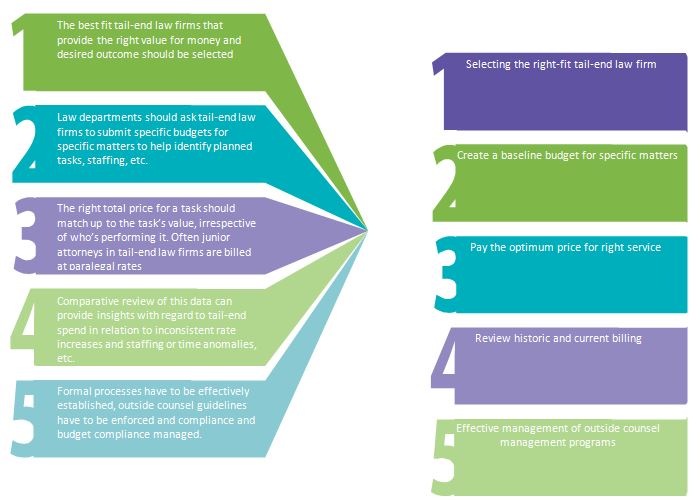

Legal Context – Differentiating factor - The legal category, like many other categories, has encountered problems related to management of tail-end suppliers and tail-end spend. This has resulted in a lot of cost-savings opportunities being lost as in-house lawyers are more inclined towards managing day-to-day legal tasks rather than effectively manage the tail-end of supplier list. As legal constitutes a high-spend category for most Fortune 500 companies, new designations such as pricing directors have come up. These roles include tasks such as ensuring optimum price for the right service and reviewing historic and current billing information. This ensures effective tail-end spend management and in-house lawyers can concentrate on the day-to-day legal tasks.

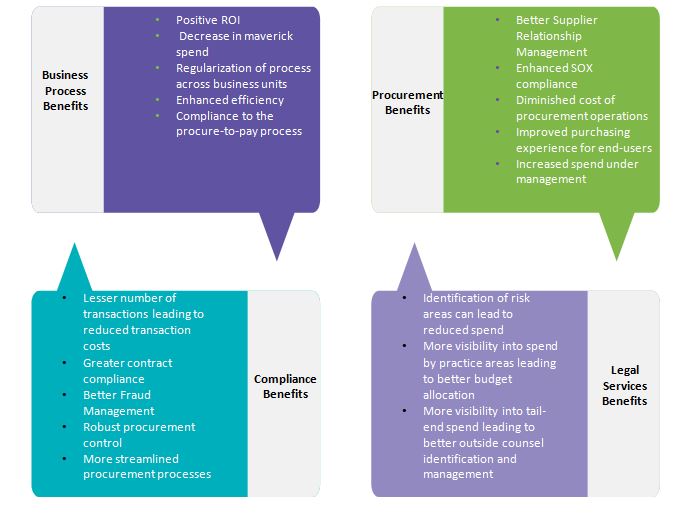

Benefits of tail-end spend management – legal services context

Procurement Action Plan

The largely unmanaged and unregulated nature of tail-end spend makes it a “grey area” among organizations, something akin to an unchartered territory, yet to be explored. However, organizations are realizing the importance of this tail-end spend and the diverse opportunities for savings hidden within it. It is gradually becoming a high-priority area for sourcing managers in large organizations as they seek “cost-savings” opportunities beyond the traditional ones.

In a company’s spend analysis, there are three main defined areas, the Managed (the main suppliers contributing the majority of the spend), the Middle (comprising of low-value spending to a large number of vendors) and the Tail (bottom-end of the spend consisting of sporadic purchases that are fragmented). After segregating the spend and breaking it down, a strategy can be created for each section. For legal services, a sourcing strategy framework can be drawn up allocating different practice areas according to the business risk attached and their relative spend. A decision can then be taken based on priority of practice areas.

Legal category managers can utilize diverse strategies to manage tail-end spend effectively such as developing a preferred list of suppliers, using e-catalogs, and building a strong bond with procurement. They can also take recourse to quality management techniques such as RCA, PFMEA and value stream mapping combined with procure-to-pay tools (such as Ariba Buyer) that help in managing the tail-end spend. With legal constituting a high-spend category for most Fortune 500 companies, new roles with designations such as pricing directors have be created to review historic and current billing information and ensure optimum price for the right service.

Conclusion

While organizations were earlier confidently managing about 40-60 percent of their spend, the situation has now changed with most large-scale organizations managing their strategic spend of 80 percent more effectively. The remaining 20 percent hangs in balance for sourcing managers. However, studies have indicated that effective management of tail-end spend can help to increase outsourcing savings potential by 1.5 times.

While managing the spend, care should be taken to assess the risk that the unmanaged tail-end spend will bring with it. In the legal context, companies are often left in the dark regarding the law firms (suppliers); this is potentially damaging to the companies’ prospects. So, as a risk avoidance measure, companies can have an in-house mechanism, a sourcing framework or a tool which will facilitate better management of this maverick or tail-end spend. This helps in delineating the practice areas based on their criticality within the organization. A methodology can then be devised to execute a plan for each spend area. So, by adopting the right approach, corporates will be better equipped to manage their tail-end spend.

Get more stories like this

Subscirbe for more news,updates and insights from Beroe