Mobile wallets to gather steam based on mutual stakeholder benefits

Abstract/Business Case

The technological advancements in the field of mobile telecommunications have influenced many facets of consumers’ lives. Mobile wallets will continue to extend this influence, offering more services and capabilities and at the same time breaking the geographical barriers. In the current scenario, mobile wallet services are at their infancy, and for the same reason banks would be imprudent to ignore them.

This whitepaper will explore the reasons for which banks should tie-up with e-wallet service providers and examine the responsibilities of each key stakeholder in the e-wallet ecosystem. It will also discuss how the engagement between banks and e-wallet service providers should work for the benefit of both the parties.

Mobile wallet services

Mobile wallet is a digital equivalent to the physical wallet that can act as a repository or vault to store digitized valuables for authorization. It can help consumers store and organize coupons, loyalty programs, payment cards and tickets. Some mobile wallets have features such as bill payment, comparison shopping, location-aware services, person-to-person payment functionality and social-media connectivity.

Based on the product types, there are primarily two types of wallets available in the industry:

- Proximity or NFC Wallets: A proximity wallet is used for authorizations and transactions involving entities which are physically close to each other. NFC wallets are typically used in scenarios such as POS check-outs in retail outlets for contactless payments owing to its higher degree of security, shorter set-up time and improved customer experience.

- Remote Mobile Wallets: In case of remote mobile wallets, the parties and entities involved in the authorization and transaction process are not physically close to each other. PayPal is one of the best examples of remote wallets. Remote wallets are used in mobile payment applications, where customers can store their credit/debit card information which can be used for multiple transactions such as online shopping and ticket booking.

Depending upon the issuing authority, mobile wallets can be of three types:

- Retailer Mobile Wallets – Retailers develop their own mobile app which features a mobile wallet capability

- FI Mobile Wallets – Banks and credit card issuers develop a mobile wallet for use by their cardholders at retail outlets

- Intermediaries – Brands such as Apple, Google and Samsung develop mobile wallets that allow usage of cards from multiple issuers

Why should banks tie up with wallet providers?

A bank can tie up with wallet providers for primarily two reasons:

- To address the challenge of serving in remote areas, banks tie up with telcos or large retailers who have distribution network. This model has been successful in many African countries.

- While online transactions have increased manifold, payments through conventional channels of net banking and debit/credit cards call for opening of several web pages. Consumers can, however, have a seamless experience with e-wallets as they provide a unified interface.

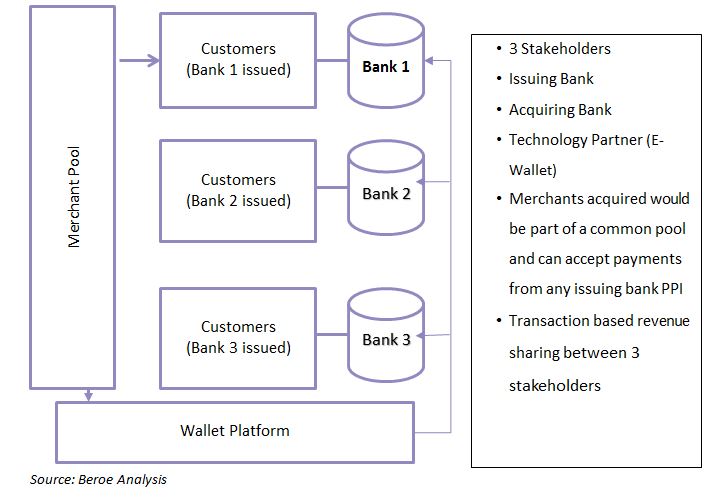

The mobile wallet ecosystem

The Wallet ecosystem consists of three vendor groups:

1. Merchant Pool

2. Wallet Player

3. Banking Player

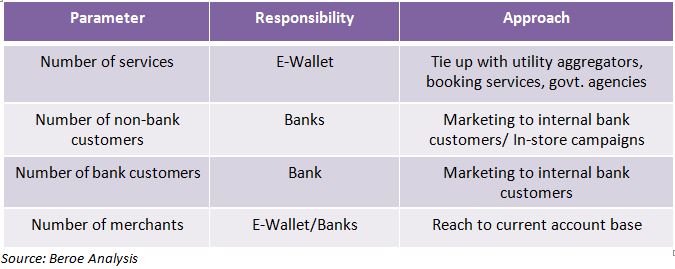

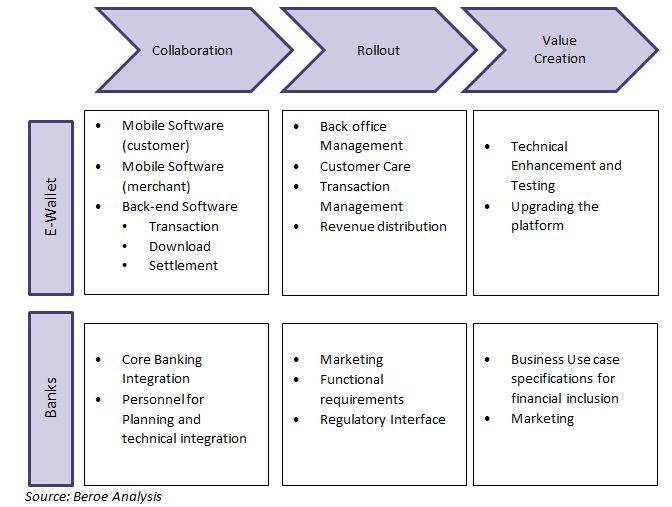

Key success factors

Responsibility matrix

The three key steps involved in the implementation and functioning of mobile wallet services are collaboration, rollout and value creation. The responsibility matrix given below clearly defines role of each stakeholder in these three steps.

Engagement between banks and e-wallet service providers

There are three distinct engagement models: Technology partnership, revenue sharing model and the joint venture model. The choice of pricing model, however, depends on the engagement with the wallet service provider and the most preferred model for a large banking organization is the joint venture model.

Technology Partnership: A bank can set up its own e-wallet system and manage its operation through support from technology providers by paying a fee for licensing, maintenance and support. In this model, banks can use the e-wallet player for running the technology and operations and pay them a fee /commission for every transaction. Here the pricing would be largely driven by the license cost for the technology and the on-going cost of operations and maintenance.

Revenue sharing with e-wallet service provider: The e-wallet provider and bank would work together with each of them having their own roles and responsibilities. The revenue earned on transactions is shared between the bank and the e-wallet service provider. Every entity in this arrangement would bear its own investment and operations costs.

Joint Venture: In this case, the bank and an e-wallet service provider would partner to set up a separate entity to manage the operations. The investments and returns are shared between the stakeholders after operational costs are deducted. This is the most preferred model for large BFSI organizations.

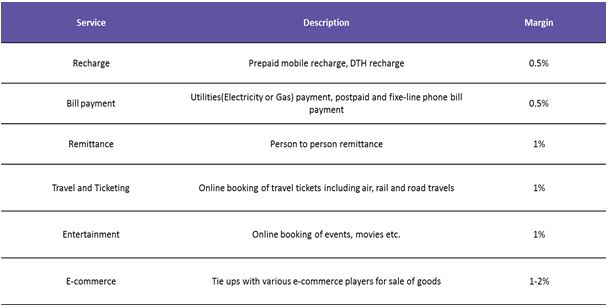

Industry margins

The industry margin for e-wallet transactions usually ranges from 0.5-1.0 percent of the transaction value. This varies depending on the transaction size and volume, and also on the application or use. However, the standard margin for players in the e-wallet transactions would be close to 0.75 percent.

Price levers

Percentage of customer acquisition: While both banks and e-wallet service providers are capable of bringing in customers into the platform, the margins or the power of negotiation would lean towards the entity that is capable of pooling in the maximum number of customers.

Share of Investments: The share of each stakeholder in the initial investment and operational costs are also the major negotiating levers. This is indirectly dependent on the engagement model.

Capability of the service provider: Other key price levers are the level of automation that the service provider can offer, network spread, geographic footprint and service capability.

Procurement action plan

Banking and financial organizations considering the deployment of a mobile wallet should be aware that there is no ‘one-size fits all’ solution in this space. The choice of engagement and deployment model varies based on aspects such as size of the organization and its current market position, maturity of the consumer mobile market, strategic intent and competitiveness of the environment.

Adopting the joint- venture model is the way forward for large banking and financial organizations that are looking at mobile wallet services from a holistic perspective. This would help banks to have a mix of best-in-class technology along with value-added capabilities and a much higher speed to market compared to other engagement models.

For the eco-system to be successful, choosing the best service provider and defining the roles and responsibilities of each stakeholder clearly is an important task for BFSI organizations.

Conclusion

Mobile wallets market is still at its infancy and it will take some time for:

- the wallet service providers to become well established

- the customer-base of financial organizations to widely adopt this service

- the market to gain momentum

Hence the banking and financial organizations who can establish a sustainable strategy are more likely to enjoy the prime-mover advantage and play an important role in the future world of transactional financial services. The key to success is to choose the best service provider and have defined roles and responsibilities for each stakeholder in the eco-system.

Get more stories like this

Subscirbe for more news,updates and insights from Beroe