Global corn markets are entering an oversupply phase in 2025–26 as production outpaces consumption, lifting inventories and rebuilding the stocks-to-use ratio after three years of tightening. Feed and ethanol demand remain resilient but are insufficient to absorb the supply expansion, limiting sustained price gains.

However, oversupply does not ensure price stability. Buyers must convert surplus into cost advantage through staggered lock-ins, selective upside hedging, index-linked contracts with flexible pricing, and diversified sourcing. While surplus strengthens negotiating leverage, logistics, policy, and execution risks remain. Effective risk management can turn surplus into cost stability and margin protection. [1], [2], [3], [4]

Introduction

The corn market is entering a clear supply-long phase as major producing regions expand output, raising global inventories and reducing the likelihood of a sustained price rally without a significant weather shock. [1], [2]

For global buyers, oversupply creates opportunity only if sourcing strategies evolve. [2] The priority is to separate global balance sheet surplus from delivered-cost risk and build flexibility across origins, freight routes, contract structures, and timing. [2] Overreliance on a single origin or spot buying can still expose buyers to basis spikes, policy changes, currency volatility, and logistics disruptions that offset weaker benchmark prices. [2], [4]

What Is Creating the Oversupply?

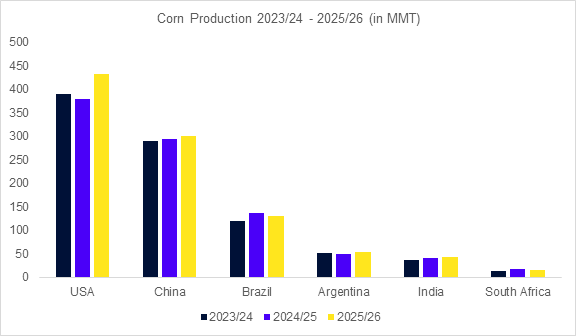

Recent seasons saw strong U.S. output driven by high yields and expanded acreage, a trend continuing in 2025. Even with slight acreage declines, supply remains ample. Elevated ending stocks limit sustained price rallies unless weather disrupts production. [1], [2], [3]

China’s revised production estimate adds significantly to global inventories. For international buyers, this reduces the likelihood of Asia-driven tightness. [1], [6]

Source: USDA

Global inventories and stocks-to-use ratios are rising after years of decline, supported by strong U.S. harvests, solid South American crops, and improved Ukrainian output.

Prices reflect this shift, with declines through parts of 2025, brief rebounds on export strength or regional tightness, and renewed softness as supply expectations improved. [2], [7], [1], [4]

Regional Friction that Can Override Global Surplus

Ukraine

Higher production supports export potential, but port throughput limitations, internal logistics bottlenecks, and security risks can restrict farm-to-port movement. The risk for buyers is not global shortage, it is execution and basis volatility. [4]

Europe

Europe remains sensitive to Black Sea flows. Corridor disruptions can cause delivered prices into Europe to strengthen independently of global benchmark softness. [4], [8]

South Africa

Domestic availability is ample, and sluggish exports have depressed prices. Interestingly, South Africa continues small yellow-corn imports into coastal markets when import parity is favorable, illustrating that local pricing can diverge from national surplus conditions. [5]

China

Even with record output, snowfall and circulation disruptions can temporarily restrict availability, affecting sentiment. [6]

Table 1: Indicators for Buyers on Regional Supply Friction

| Country | Outlook | Procurement Indicators |

|---|---|---|

| Global | Higher world carryover led by China’s revised output | Lower probability of global shortage |

| USA | Season totals look strong, weekly prints could be trimmed | Benchmark upside is limited without a market shock |

| Ukraine | Demand is firm but logistics/security constrain flow | Basis and execution risk can spike delivered cost |

| South Africa | Big domestic supply, exports behind target, prices depressed | Good buying window now; watch export catch-up |

| China | Snowfall is expected to slow corn movement into trade channels | Local availability can tighten temporarily even when annual output is high |

| Europe | Europe remains sensitive to Black Sea availability and corridor disruption | Delivered cost into Europe can dissociate from global surplus if Black Sea logistics tighten |

Strategic Implications for Buyers

- Oversupply improves negotiating leverage, but does not eliminate delivered-cost risk

A looser balance sheet strengthens buyer negotiating power and limits sustained benchmark rallies. However, procurement risk shifts from “availability at any price” to “delivered-cost volatility.” [2], [4], [8]

Market pricing now operates across three distinct layers:

- Benchmark (futures/flat price): Influenced by global supply and U.S. stocks.

- Basis (origin differential): Driven by logistics, port flow, and local circulation.

- Execution (physical delivery risk): Affected by congestion, security, and infrastructure.

- Origin diversification becomes a procurement requirement

In a surplus market, focusing on the cheapest origin may seem efficient. A diversified origin strategy protects against localized demand shocks and ensures supply continuity. [2], [4], [5], [8], [9]

- China and Europe illustrate why local dynamics must be managed separately from global supply narratives

China and Europe highlight the need to manage local conditions separately from global balances. Internal Chinese circulation and Black Sea corridor risks can distort delivered pricing despite a global surplus. [6], [7], [4]

- Supplier and contract strategy should be redesigned around resilience and responsiveness

Surplus periods offer the best opportunity to renegotiate commercial terms. Buyers should secure:

- Guaranteed allocation volumes

- Multi-window price setting

- Hybrid fixed/floating structures

- Collar mechanisms

- Stronger force majeure clarity

- Logistics transparency and penalty clauses

The goal is resilience and responsiveness rather than purely lowest headline price. [2]

Table 2: Sourcing by Corridor

| Corridor | Primary Risk | Best Practice |

| Black Sea – EU/MENA | Port/logistics constraints + security risk | Flexible delivery terms + alternate sourcing |

| South Africa – Southern Africa | Export acceleration risk into April 2026 | Layer purchases |

| US – Global | Futures moves on macro | Pre-approved buy triggers + hedge discipline |

| Asia Demand Pockets | Rapid reactivation when economics work | Maintain optional suppliers and shipping slots |

Source: FastMarkets, Zawya, The Western Producer

Recommended Strategic Posture for 2025/26 into Early 2026

• Secure continuity through layered coverage rather than single-point locking. [2]

• Preserve optionality via multi-origin qualification, substitution rights, and flexible shipment windows. [2]

• Monitor export pace and corridor performance as the primary early-warning indicators of tightening risk. [2], [4], [5]

• Exploit surplus conditions to renegotiate stronger commercial terms, improving resilience at minimal incremental cost. [2]

Conclusion

The U.S. is producing at record levels with rebuilding stocks, global inventories are lifted by China’s higher output estimate, and exports are active without tightening the balance. [1], [3] Yet global buyers should not confuse “surplus” with “no risk.” [2] The practical procurement challenge is delivered cost, especially where logistics, security, and export timing can create sharp basis moves. [4], [5], [8] The optimal strategy in this environment is layered coverage with strong optionality: lock continuity, keep tactical flexibility, separate benchmark hedging from basis control, and use contract terms that defend execution in the lanes most exposed to disruption. [2], [4]

References

[1] U.S. Department of Agriculture, “World Agricultural Supply and Demand Estimates (WASDE),” Jan. 2026.

[2] The Western Producer, “world-corn-production-outpaces-rise-in-demand,” Jan. 2026.

[3] U.S. Department of Agriculture, National Agricultural Statistics Service, “Crop Production (Corn): 2025 results incl. production, yield, planted and harvested area,” Jan. 2026.

[4] Reuters, “Russian attacks on Ukrainian ports cause drop in food exports,” Dec. 2025.

[5] Zawya, “South Africa’s maize export activity continues, but at a slower pace,” Feb. 2026.

[6] MySteel, “China Grain Market Review:Corn price enters a fluctuation stage

“, Jan. 2025.

[7] UkAgroConsult, “EU raised wheat and corn harvest estimates” Dec. 2025.

[8] S&P Global Commodity Insights, “Logistical constraints shift EU corn import dynamics, Ukraine loses share” Feb. 2026.

[9] Th Daily Star, “Bangladesh resumes US corn imports after 8 years”, Jan. 2026.

About Beroe

Beroe is a global SaaS-based procurement intelligence and analytics provider. We deliver intelligence, data, and insights that enable companies to make smarter sourcing decisions – leading to lower cost, reduced risk, and greater profits. Beroe has been a trusted source of intelligence for more than 15 years and presently partners with 10,000 companies worldwide, including 400 of the Fortune 500 companies.

Learn more about Beroe https://www.beroeinc.com

Author

Neha Unnikrishnan

Related Reading

10 Mar, 2026

AI That Actually Works: Why MCP Integration is a Turning Point for Procurement Data