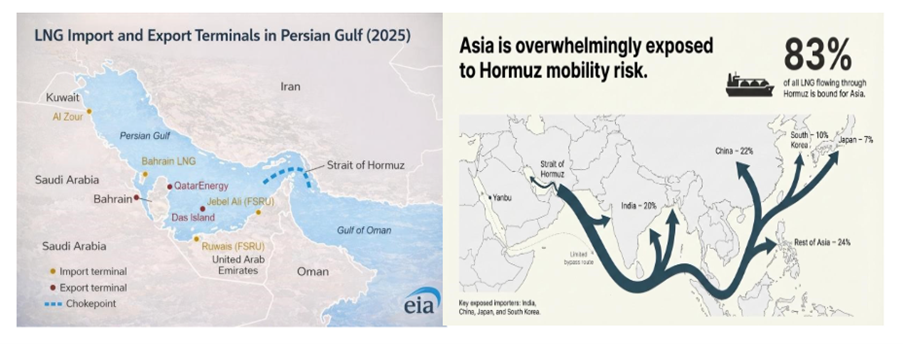

The late-February 2026 escalation involving U.S.–Israel strikes on Iranian assets and related maritime security incidents in the Strait of Hormuz region causes significant concerns for procurement teams. Given that the Strait carries approximately 20–25% of global seaborne crude flows (~20 million barrels per day) and ~20% of global LNG trade, corridor concentration introduces structural pricing sensitivity across crude, LNG, freight, and marine insurance markets, independent of sustained physical supply interruption.

(Source:www.eia.gov)

Introduction

This article frames corridor stress as a sourcing leverage inflection point. It examines how energy-linked volatility transmits through commodity, freight, and insurance curves – and how those movements reshape commercial power dynamics across supplier portfolios.

Rather than focusing on price direction alone, Beroe’s analysis centers on leverage migration: where cost amplification is structural, where margin expansion may emerge, and where information asymmetry influences negotiation posture.

For procurement and sourcing leadership, the relevance lies in anticipating commercial repositioning before pricing norms re-anchor. The objective is to strengthen cost transmission visibility, calibrate contract architecture, and evaluate supplier power redistribution under widened volatility conditions.

Strategic sourcing maturity determines whether volatility translates into margin erosion or leverage recapture.

Corridor Concentration & Structural Exposure

Quantified Energy Transit Sensitivity

• ~20–25% global seaborne crude via Strait of Hormuz

• ~20% global LNG transit share

• Freight rerouting delta modeled band: +10–40% distance impact depending on route

• Transit extension modeled band: +10–20 days

• Marine insurance premium widening precedent: +5–25% under historical corridor stress periods

• Baltic freight sensitivity demonstrates multi-percentage upward movements under elevated corridor perception risk

Modeled volatility bands are calibrated against observed market reactions during prior corridor and supply-concentration stress episodes, including the September 2019 Abqaiq–Khurais disruption and the 2019 Strait of Hormuz tanker incidents. Precedent reference points include publicly reported Brent repricing, Baltic tanker index movements, and Lloyd’s marine insurance bulletins during those periods.

Critical differentiation must be made between structural cost amplification (energy or freight driven), margin opportunism embedded within escalation cycles, and liquidity-driven defensive repricing.

Cost Transmission Observability Gap: The variance between actual supplier cost inflation and perceived cost inflation in buyer negotiations. Where observability is weak, leverage is conceded.

Transmission Modeling Cases (The following scenarios translate historical corridor stress patterns into structured exposure ranges for sourcing assessment)

Case A – Stress Pricing Without Flow Restriction

• Brent expansion band: +5–15%.

• Freight uplift: +3–10%.

• Temporary insurance hardening: +5–40%.

• Supplier escalation timing cycle: 30–60 days.

Case B – Partial Transit Restriction / Rerouting

• Effective voyage distance delta: +10–40% (routing dependent)

• Transit delta: +10–20 days

• Bunker cost exposure sensitivity: +8–15%. (fuel price + voyage duration interaction)

• Insurance hardening band: +15–40% (severe escalation scenario range

• Commodity ripple: steel, petrochemical feedstocks, fertilizers, energy-intensive inputs.

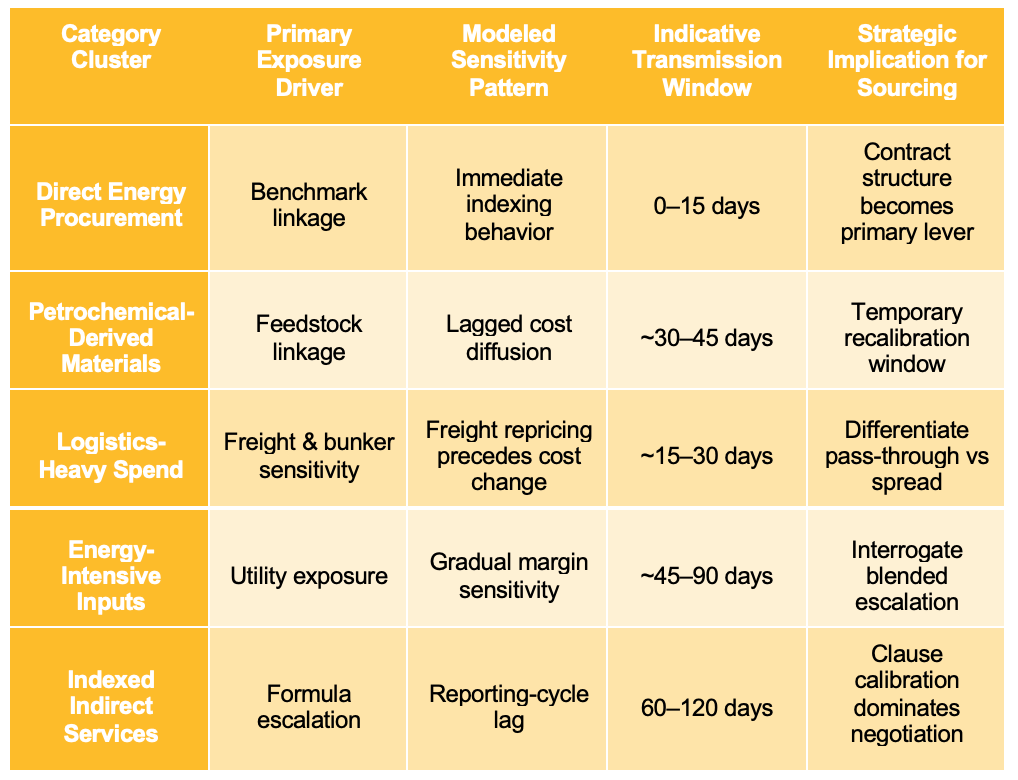

Category-Level Intelligence Modeling

Energy corridor stress does not transmit uniformly across spend architecture. Historical volatility episodes suggest differentiated sensitivity timing based on energy intensity, freight dependence, and contractual index linkage structure.

Methodology Note: Transmission windows derived from analysis of historical corridor stress episodes (2019–2022) tracking freight, commodity, and insurance repricing timelines.

Managing Energy Supply Risks Through Strategic Sourcing

Energy corridor stress rarely requires immediate structural overhaul. However, historical volatility episodes suggest sourcing architecture may benefit from selective recalibration when pricing bands widen and leverage dynamics shift. Rather than operational intervention, the opportunity typically lies in reassessing portfolio structure, supplier positioning, and commercial design.

A. Portfolio Re-Segmentation Under Volatility

Periods of elevated energy sensitivity may warrant reassessment of category clustering based on energy intensity exposure, freight dependency concentration, and index-linkage structures. In certain phases, sourcing calendar sequencing itself can become a lever: advancing or deferring bid cycles –where commercially viable – may influence anchor pricing before volatility bands normalize.

Where volatility exposure is materially high, selectively advancing renewal cycles for energy-intensive materials by approximately 30–45 days may preserve negotiation leverage ahead of further band expansion.

B. Supplier Power Rebalancing

Volatility does not affect all suppliers uniformly. Observationally, suppliers may exhibit differentiated behaviors – pricing opportunism under widened bands, genuine margin compression via input diffusion, freight pass-through without structural cost change, or liquidity-driven posture. Distinguishing these patterns can clarify whether escalation reflects structural movement or defensive positioning. In certain cases, calibrated transparency dialogue (including selective open-book) may rebalance posture where narrative exceeds cost reality.

For Gulf-linked contracts or energy-sensitive inputs, initiating a structured escalation clause review within 15 business days of a volatility event can strengthen negotiating posture before cost narratives harden.

C. Contract Architecture Recalibration

Energy-linked volatility can highlight latent asymmetry in contract design. Index mechanisms, duration assumptions, and escalation triggers may merit review where widened bands expose imbalances. Hybrid frameworks – combining stability elements with calibrated volatility responsiveness – have often proven more balanced than rigid fixed or purely floating constructs. The implication is not urgency to renegotiate, but disciplined refinement of structural resilience over time.

In categories with corridor exposure, mapping supplier inputs with greater than 60% Gulf transit dependency can clarify hidden concentration risks before escalation mechanisms are activated.

D. Structural Supplier Mix Considerations

Corridor concentration sensitivity can increase scrutiny on geographic exposure and route dependency. Supplier evaluation frameworks sometimes incorporate energy intensity weighting, transit corridor exposure scoring, and balance-sheet resilience indicators. Geographic diversification may introduce cost premiums; however, in selected categories, structural redundancy can mitigate asymmetric exposure. The strategic decision often lies in balancing efficiency optimization with exposure concentration sensitivity.

During pronounced volatility spike phases, delaying long-term fixed-price commitments – where contractually feasible – may reduce risk of locking in temporary risk premia before markets normalize.

Key Executive Takeaways on Energy Supply Volatility

- Corridor concentration often influences market pricing dynamics before physical flows are materially constrained; commercial positioning may adjust in anticipation of disruption rather than confirmed interruption.

- Expanded volatility bands can widen negotiation dispersion; in past cycles, price divergence has reflected variability in risk assessment as much as underlying cost transmission.

- Where input cost visibility is constrained, escalation narratives can outpace verifiable cost movement; information symmetry frequently influences leverage retention.

- The sequencing of sourcing activity during volatility phases can materially shape commercial anchors; renewal timing, bid cadence, and index reset alignment may affect price outcomes before markets re-stabilize.

- Suppliers with diversified input sourcing or hedged exposure may exhibit differentiated sensitivity profiles relative to corridor-concentrated producers; understanding these asymmetries can clarify whether escalation reflects structural cost change or precautionary positioning.

- Liquidity conditions within the supply chain influence commercial posture; capital-constrained suppliers may prioritize cash flow stability, while well-capitalized suppliers may emphasize margin preservation.

- Internal alignment speed across finance, sourcing, and leadership materially affects response quality; early coordination improves proportional response and reduces reaction-driven decision risk.

Closing insight: In corridor-concentration environments, advantage rarely derives from predicting disruption. It more commonly stems from recognizing early leverage shifts and recalibrating sourcing architecture with measured discipline before volatility bands normalize.

References

EIA (2025), “Amid regional conflict, the Strait of Hormuz remains critical oil chokepoint,” U.S. Energy Information Administration, https://www.eia.gov/todayinenergy/detail.php?id=65504

EIA (2023), “The Strait of Hormuz is the world’s most important oil transit chokepoint,” U.S. Energy Information Administration, https://www.eia.gov/todayinenergy/detail.php?id=61002

EIA (2025), “About one-fifth of global liquefied natural gas trade flows through the Strait of Hormuz,” U.S. Energy Information Administration, https://www.eia.gov/todayinenergy/detail.php?id=65584

IEA (2025), “Gas 2025 – Summary,” International Energy Agency, https://www.iea.org/reports/gas-2025/executive-summary

World Bank (2025), Commodity Markets Outlook, October 2025 Edition, World Bank Group, Washington, DC, https://openknowledge.worldbank.org/entities/publication/d08d3ee8-e38a-4f02-8ade-95b9c6075c0b

Reuters (2026), “Iran conflict disrupts global shipping as tankers are stranded, damaged,” Reuters News Service, 2 March 2026, https://www.reuters.com/business/energy/iran-conflict-disrupts-global-shipping-tankers-are-stranded-damaged-2026-03-02/

Reuters (2026), “Global oil, gas shipping costs surge as Iran vows to close Strait of Hormuz,” Reuters News Service, 2 March 2026, https://www.reuters.com/world/middle-east/middle-east-oil-shipping-costs-surge-all-time-high-us-iran-conflict-intensifies-2026-03-02/

Reuters (2026), “Three tankers damaged in Gulf as US–Iran conflict escalates,” Reuters News Service, 1 March 2026, https://www.reuters.com/business/energy/three-tankers-damaged-gulf-us-iran-conflict-escalates-2026-03-01/

Reuters (2026), “Market analysts react to US–Israel strikes on Iran,” Reuters News Service, 28 February 2026, https://www.reuters.com/business/energy/market-analysts-react-us-israel-strikes-iran-2026-02-28/

Author

Imran Firoz

Related Reading

10 Mar, 2026

AI That Actually Works: Why MCP Integration is a Turning Point for Procurement Data